Scent of light

Download Pdf

There are many tasty dishes that are simple to prepare. However, the ingredients are extremely important, as is the correct combination of them. The same applies to the stock markets. Below are the ingredients for a tasty and healthy dish. With few calories and potentially some capital gains.

1/4 of dramatic geopolitical event whose peak has passed

1/4 of nice strong inflation, from transient factors

1/4 clap of solid consumer savings and a pipeline of strong infrastructure investment

1/4 interest rates normalising and a robust financial system

Supportive governments, as much as required.

Mix everything well, no rush. Dramatically increase lower wages before baking.

Take care to burst any “growth” bubbles that arise during baking.

Serve with depressed traditional market valuations, on a bed of fresh recession and stagflation fears.

It should be doused with something sparkling and young, like post-pandemic, vintage 2020 or 2021 spending appetite.

Taste possibly after Macron’s victory and before the dividend wave coming in May.

Enjoy.

CardYes, CardNo

An experienced friend of mine has expressed his perplexity about Nexi’s performance. After reaching €18 per share, the stock has halved in a few months, with constant and worrying weakness. Anyone who knows the market well, knows that prolonged phases of weakness can hide serious problems, and so he wondered if there might be something rotten in the stock.

Intrigued, we took a look at the company. An in-depth analysis would require more time, particularly on a sector that is extremely popular with the market and as such, ignored by us.

What emerges from our initial analysis is that:

1) The weakness of the stock seems to reflect the weakness of the sector. Below is the chart showing Nexi, Worldline, Adyen and Paypal at one year. Adyen and Paypal belong to a different league in terms of quality, but we see that they too have been subject to strong derating.

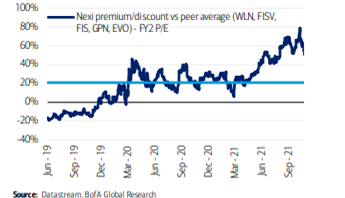

2) At the beginning of the year, the company was showing a considerable premium to its direct peers as seen below. Today the premium has partially reduced.

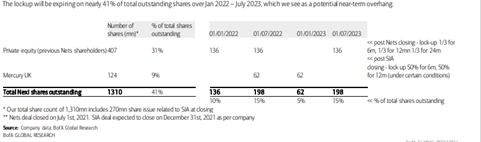

3) Nexi has a number of expiring lock-ups ahead of it which could create a substantial sales flow over the next 12 months. Below is a mirror showing that 136m shares in lock-up have already been released since January.

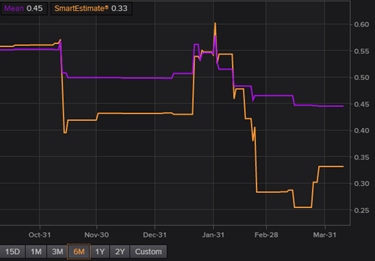

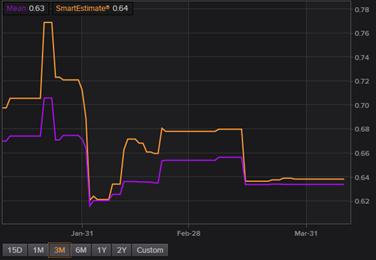

4) The company’s guidance released in conjunction with its Q4 results indicates that it is struggling to meet its targets, which in turn perhaps indicates an increase in competitiveness in the sector. Below are the changes in EPS estimates for 2022 and 2023 in recent months. Couple this with valuations that at the start of the year reflected a lot of positivity about growth and substantial, though to date unceremonious, debt, and you can understand why some have reduced exposure

Today the company is worth around 10x 2023 EBITDA (EV/EBITDA) in line with its direct peers (companies like Adyen and PayPal have different characteristics and deserve premium valuations over Nexi). The valuation of the stock and the sector cannot be considered expensive today and its rerating or derating will be linked to whether or not earnings growth is confirmed. Given the assumption that digital transactions increase earnings growth will depend in the short term on competitive pressures in the sector and, a little further down the line, on any risks from technological change. As in all bubbles, first comes the massive and seemingly incomprehensible derating and then, gradually, the problems emerge. We believe that stocks related to bubble issues should be treated with great caution because the adjustment process usually takes years, not months. The same optimism that creates bubbles then leads to a glut of players, acquisitions made at optimistic prices, regulatory attention and stimulus for technological change. And it often goes from being shamefully expensive to shamefully cheap.

CardYes, CardNo(2)

We country managers find the digital payments sector quite complex. There are so many players and roles. Issuer, acquirer, gateway, processor… Only apparently there are large unassailable players. In reality, excluding issuers (VISA and etc) the other roles are vulnerable. An example comes from the small Adyen that in a few years has become a colossus, a cut above the rest, thanks to a faster and more efficient software and an intelligent strategy.

Then there is another problem. And this also concerns issuers. The future of payments is not necessarily tied to the debit/credit card circuit. Merchants do not like interconnection costs and technology is improving. ACH (automated clearing house) and BNPL (Buy Now Pay Later) models are interesting alternatives with some shortcomings. Blockchain circuits such as cryptocurrencies could also be an alternative, although they also present some problems, of cost and speed. However, things could change quickly.

In conclusion, we are not sure that securities such as VISA or Adyen itself, leaders in their respective markets, deserve extremely generous valuations as they do today, given the many risks in the sector.

Back