The Future is electric

Electric mobility funds have fared poorly since the middle of last year mainly on concerns about China flooding the market with cheap EVs, with some ETFs declining by as much as 30%-35% since July.

This looks overdone, partly the result of the pendulum in investor sentiment between euphoria and pessimism.

The future of the world remains squarely electric, with the electric mobility megatrend here to stay, supported by environmental concerns, government incentives, technological progress (making EVs more affordable and better performing), infrastructure development and favourable consumer preferences.

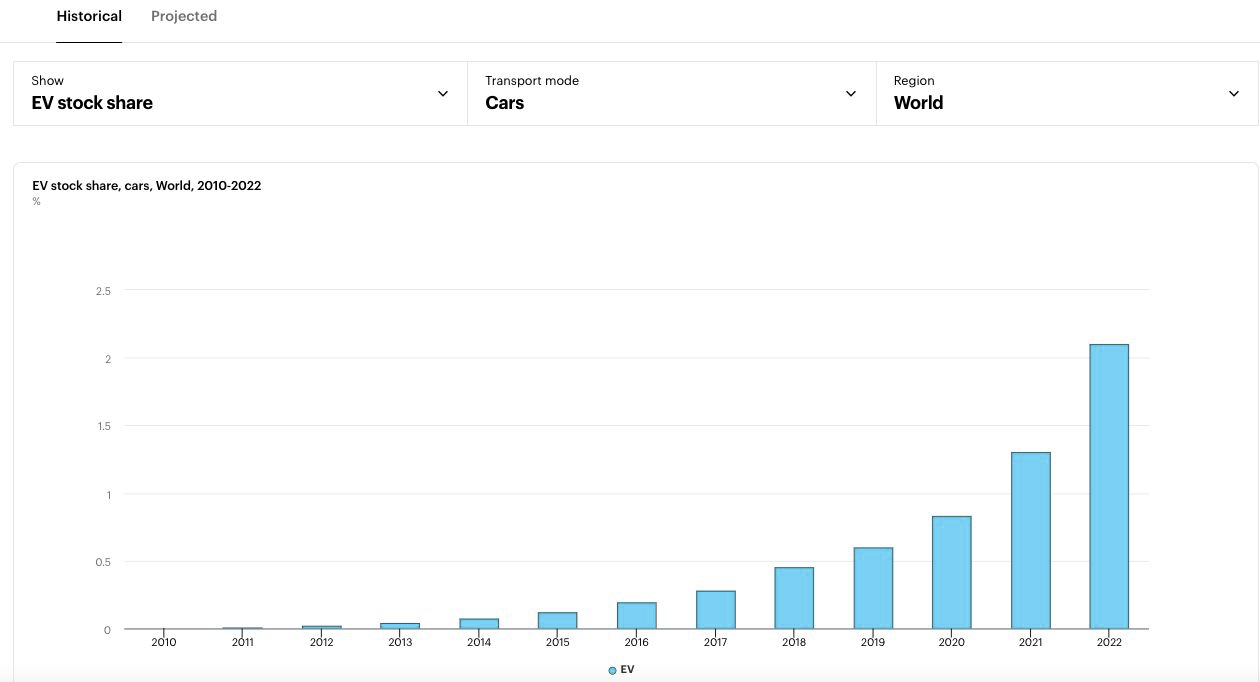

Global market-sales share for electric vehicles is growing fast but remains at an average of ~15%, while global market-penetration is still on average ~2.0% (source: IEA).

In other words, e-mobility has not even embarked on the fast-growth and fast-adoption stage of the S-shaped penetration curve but some investors have seemingly already given up.

Paraphrasing MIT’s Malone, every technology breakthrough takes twice long as expected but half as long as the industry and the market are prepared for. And what the market is not yet prepared for and therefore not yet pricing in e-mobility stocks is the under-capacity scenario we still expect for the battery space, which should give key battery players stronger pricing power, better margins/earnings and higher valuations.

Yet not all that shines is gold….and not all e-mobility funds are equally attractive or equally effective in generating returns while protecting capital across cycles.

Our Electric Mobility Value Niche is a global equity fund that offers exposure to the EV battery ecosystem, investing in electric mobility players not recognized as such by the market and thus with potential for significant re-rating. The battery ecosystem represents 75% of the portfolio.

The chart below shows performance since inception for Niche AM’s E-mobility Value Niche fund vs ETF peers BATT and LIT. Yes, the latter has generated slightly higher returns over the period, but it has achieved so with double the volatility and a drawdown 3.5x as high.

At Niche AM we believe investment is as much about generating returns as about controlling risk, which we do by:

1. adopting a deep-value approach, as the price paid for the asset is the main determinant of its downside risk – this approach eliminates the risk of investing into a bubble

2. avoiding leverage at companies held in the portfolio

3. building a highly diversified portfolio

4. implementing an ESG-responsible approach, which reduces regulatory and political risk.

Within this framework market-timing, always challenging if not impossible, becomes less warranted.

For details on our EMVN fund see here.

This is a marketing communication for institutional investors. Please refer to Fund Prospectuses & KIDs before making any investment decision.

For any questions email us on: info@nicheam.com

Follow us on LinkedIn: www.linkedin.com/company/niche-am

Back