Developed or still emerging?

According to Nobel Prize-winning economist Simon Kuznets, countries can be categorized into four types: developed, undeveloped, Japan and Argentina. Perhaps he should have added a fifth type: South Korea.

South Korea boasts the 14th largest economy globally and ranks in the top decile worldwide for GDP per capita. It’s a member of the OECD since 1996, while the IMF has classified it as an advanced economy already in 1997. Its stock market is the 12th-biggest globally, with a capitalisation of about $1.8trn, ahead of the likes of Italy and even Switzerland. The country leads the world in R&D investment relative to GDP. The West heavily depends on South Korea for semiconductors, smart phones and smart TVs, while greatly enjoys its pop music, films and food.

Since the 1980s, the country has also transitioned into a modern Western-like democracy, curbing corruption and limiting the economic and political dominance of chaebols.

And yet, despite possessing nearly all the hallmarks of a developed market, MSCI has once again, back in June, reclassified South Korea as an “emerging market”. Click on image below for details.

MSCI is primarily concerned about the convertibility of the Korean won in the currency market and is also unhappy with the full ban on short selling reintroduced in November 2023.

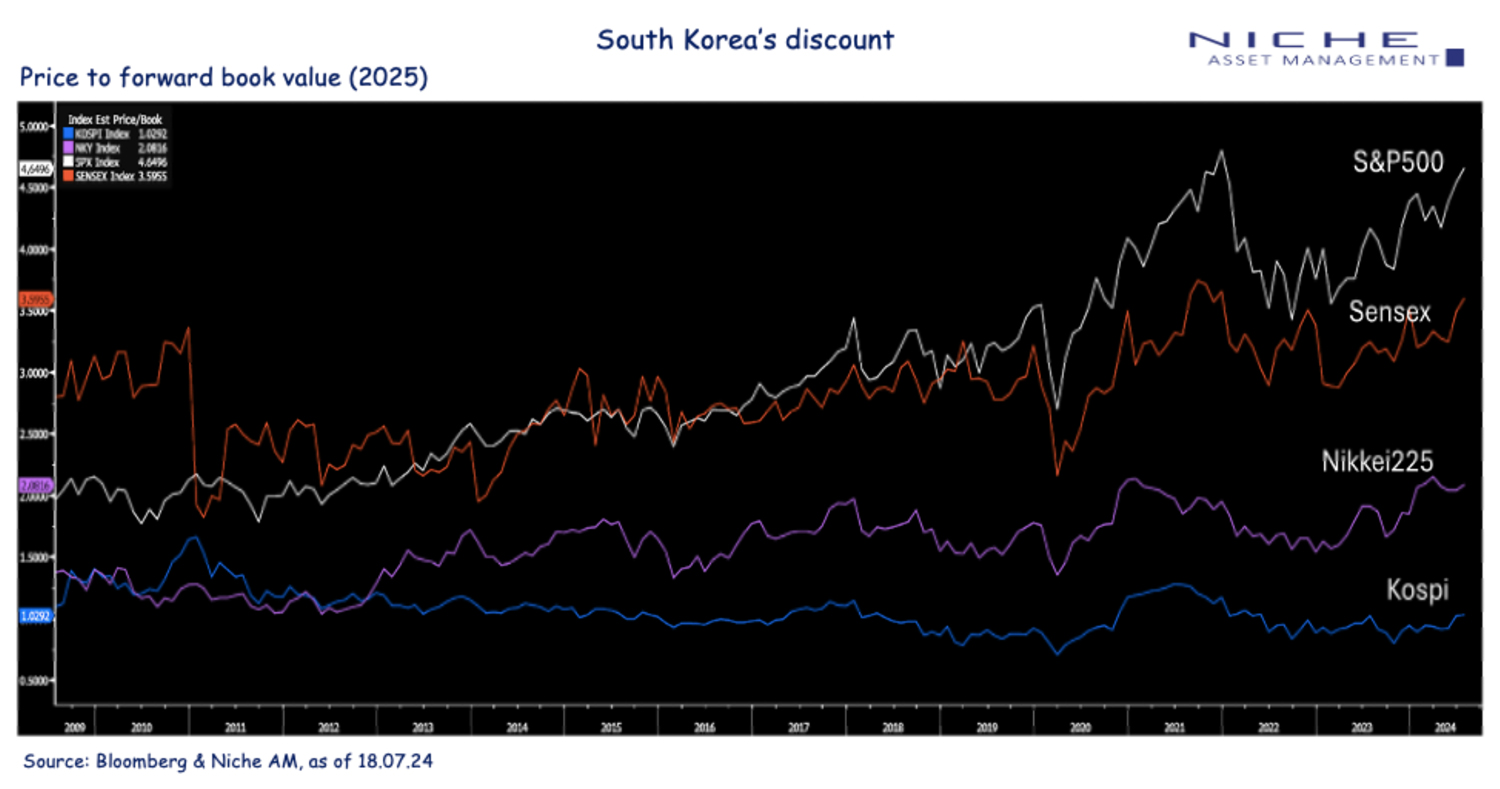

MSCI’s classification as emerging market probably contributes to what is known as the South Korea "discount" – a term describing the underperformance/undervaluation of local stocks compared to other global equity benchmarks.

A discount which is probably also the result of other factors, such as an exaggerated perception of the military threat from North Korea (are investors not investing in German stocks due to its proximity to Russia?); poor corporate governance within South Korean conglomerates; and the inaccessibility of South Korean stocks for non-domestic retail investors.

While we can't predict when (or even if) MSCI will upgrade South Korea to "developed market" status, it's worth noting a couple of things.

First, the country is already, albeit gradually, easing restrictions on the currency market (where the heavy regulatory focus reflects the comprehensible hyper-vigilant mindset forged in the wake of the capital flight and won collapse witnessed during the Asian Financial Crisis of 1997).

Second, while inclusion in MSCI’s Developed Market index is estimated by Goldman Sachs to potentially lure some US$46bn-56bn of fresh capital into South Korean assets, an investment case for South Korea doesn't need to hinge on MSCI's reclassification.

As value investors, our investment case for South Korea is primarily based on valuation.

As of today, approximately 29% of the Korean listed market trades below tangible asset value. This percentage increases to around 65% when considering the number of companies rather than their market weight.

This misvaluation significantly impacts all companies, particularly medium and small caps (which in fact have basically not moved over the past decade).

South Korea offers a compelling alternative to the Chinese stock market. Probably much more compelling than arguably expensive India. Despite China's poor stock performance in recent years, South Korea is trading at about 9.9x 2024 earnings, vs. China’s 11.7x circa (and India’s >23x).

And this lower valuation comes without all the risks related to China, such as policy uncertainty, deglobalization / reshoring / friendshoring, Taiwanese tensions, a real estate bubble, and a stressed financial system.

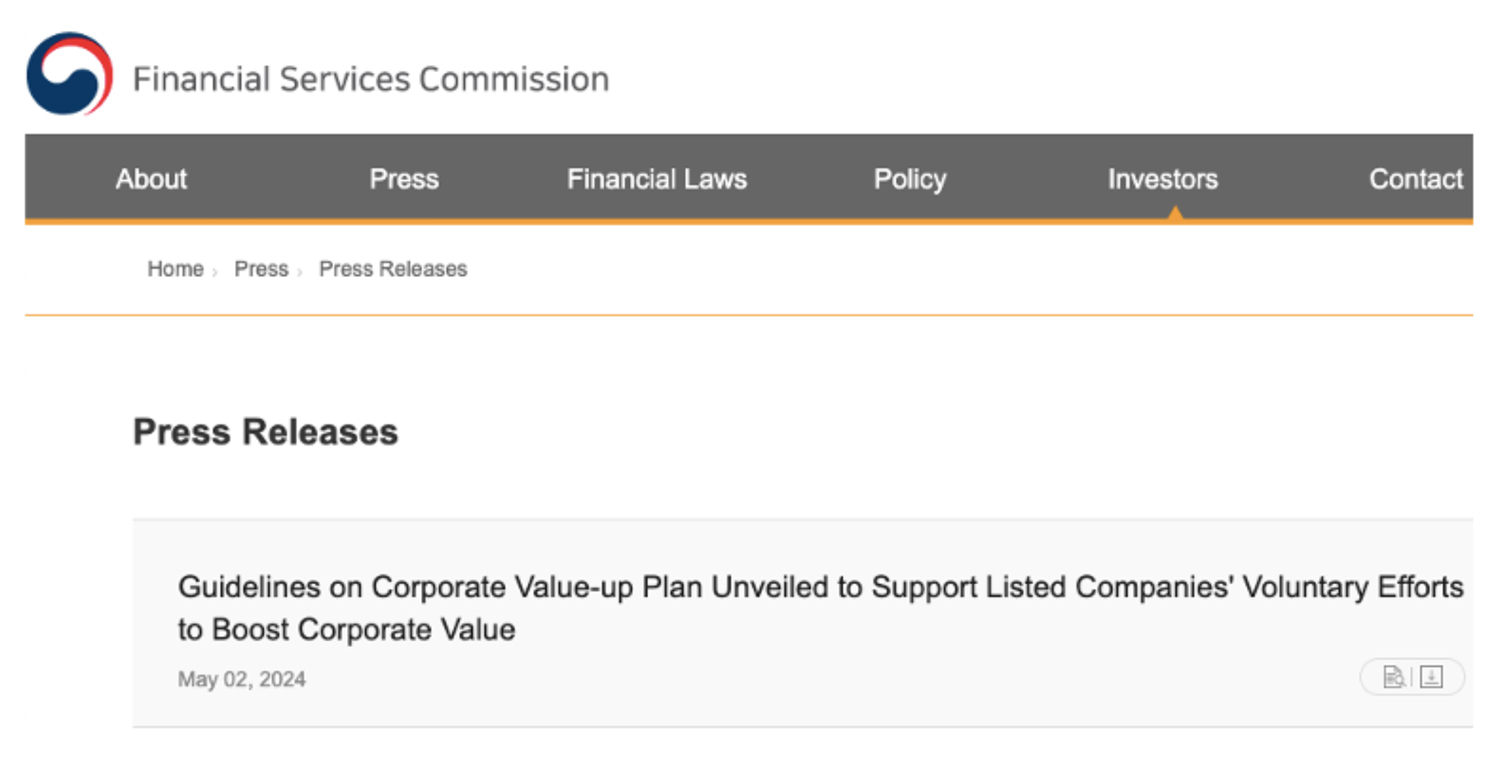

Imminent policy measures should gradually help close the South Korean discount. Last February, the government announced the so-called Value-up Plan, final details of which should be available shortly.

Click on image below for details.

The plan will allegedly offer tax incentives to companies that implement measures to enhance investor communication and governance, with the aim of focusing investor attention on hundreds of undervalued companies.

It appears that participating companies would be able to tax deduct 5% of any increase in shareholder returns (i.e.: dividends and buy-backs) over and above the average of the previous three years. There would also be a reduction in personal tax on dividend increases, from 45% to 25% (or from 14% to 9% for small shareholders).

For Chaebols and family businesses that typically do not distribute dividends, these measures would represent an opportunity to issue extraordinary dividends over the next two years. Even large companies will be motivated by shareholders to increase their currently low payouts.

Companies that join the program and meet the plan’s minimum communication and governance standards, would apparently be included in specific indices and become thus eligible for investment by pension funds and insurance companies.

![]()

At Niche AM, we view South Korea’s companies as exceptionally compelling opportunities, both in terms of valuation and business fundamentals.

This is the reason why our NEF Ethical Global Trends SDG fund is significantly overweight South Korea, which represents 11% of the portfolio vs the meagre 1% held by benchmark MSCI ACWI Value. This overweight position sharply contrasts with NEF EGT's minimal 0.13% exposure to China, exposure which the fund has been actively reducing since 2022, when Niche AM adopted the policy of not investing in countries deemed as autocracies by Freedom House.

NEF Ethical Global Trends holds 33 South Korean stocks, trading at an astonishingly low multiple of around 7x earnings (yes, 7x—it’s not a typo) and well below tangible book value.

These companies aren’t just cheap. They are also companies with good ESG profiles, which are making a positive contribution to achieving the UN’s Sustainable Development Goals (consistent with the classification of the fund as an Article 9 SFDR).

And we know this because at Niche AM we conduct rigorous sustainability analyses, both quantitative and qualitative. Once in the portfolio, we ensure that companies demonstrate a consistent improvement in sustainability over time. If a company deviates from its improvement trajectory, we actively engage with management to understand and address that deviation directly. If the deviation is not justified and/or the company does not return onto an improving trajectory within a reasonable time, the stock is sold as soon as allowed by market conditions.

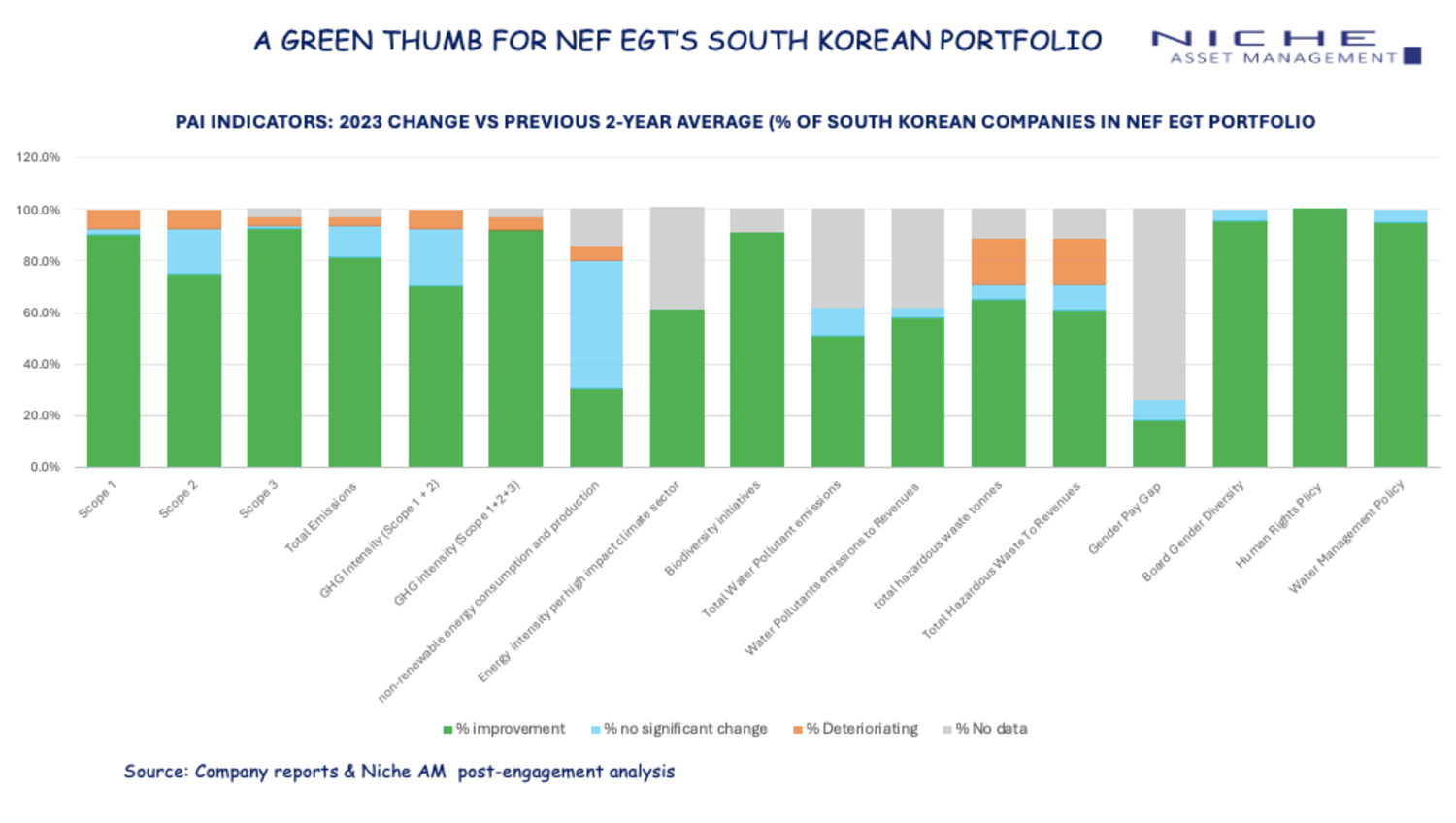

The 33 South Korean names in our NEF EGT portfolio have been carefully selected based on this comprehensive sustainability process. The selection was made from an initial pool of approximately 150 South Korean firms, which themselves were shortlisted from around 2,500 listed companies on the basis of valuation and liquidity.

The chart below illustrates the mostly improving sustainability performance and responsiveness of South Korean companies in NEF EGT’s portfolio between 2021 and 2023.

As value investors, we don't wait for "catalysts" before investing, primarily because once a catalyst becomes apparent or obvious, it is often too late to invest.

However, if pressed to identify potential catalysts for South Korean stocks, we would mention the MSCI reclassification discussed above and (probably more impactful in terms of upside potential), any reform in North Korea on the lines, for example, of what took place in China or Vietnam over the last 20 years.

Any change in the northern neighbour represents an opportunity to which the market is currently assigning zero probability, and it would hugely benefit this segment of NEF EGT’s portfolio, predominantly composed of companies deeply integrated into the peninsular economy.

See here for further details on NEF Ethical Global Trends SDG.

Follow us un LinkedIn

This is a marketing communication intended exclusively for institutional investors.

Refer to Fund Prospectuses & KIDs before making any investment decision.