Goodbye plush toys?

Download Pdf

We grew up with the idea that the democratic world was well organised. Entrusted to capable and responsible men and institutions. Balanced and fair. That governance was fair and well defined. But this is not the case. The level of incompetence, ignorance, inefficiency and dishonesty is staggering. Many of the international institutions that claim so much credibility are in fact inept and useless hulks, at the mercy of economic and political interests. In such a context, it is not surprising that organised greed in the form of corporations/businesses prevails, controlling the ganglia of power and the very lives of billions of people.

The only glimmer of light for today’s democracy is to analyse its alternative: autocracy. This renders the current defects of democracies meaningless, however imperfect, is the only adequate organisational form. It must be improved to make it sustainable.  A democracy that does not represent the demands of the majority of citizens, inevitably leads to nationalistic regurgitation. We have seen this recently in the USA, as well as in Europe and elsewhere. Economists such as Stiglitz, Krugman and Korten, who saw risks to democracy in an excessively savage capitalism, have often been sidelined. Today they are being re-read and reappraised.

A democracy that does not represent the demands of the majority of citizens, inevitably leads to nationalistic regurgitation. We have seen this recently in the USA, as well as in Europe and elsewhere. Economists such as Stiglitz, Krugman and Korten, who saw risks to democracy in an excessively savage capitalism, have often been sidelined. Today they are being re-read and reappraised.

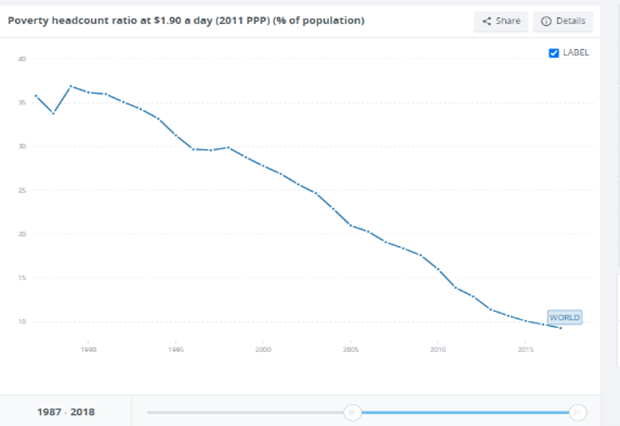

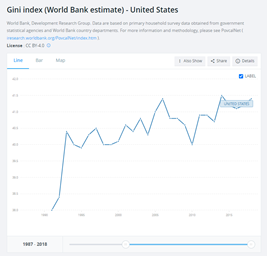

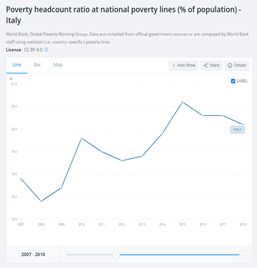

It cannot be denied that globalisation has had positive effects. Thanks to it, much of the poverty in emerging countries has been eradicated (see graph above) and the average age of life has risen considerably. However, its exaggeration has had a cost for the West that is now proving excessive, particularly for the weakest and most numerous, as can be seen in the two graphs above. This cost has risked plunging the West into the darkness of  autocracy.

autocracy.  To open a long period of stalemate in the path of progress, like the Middle Ages. However, Covid and the Ukrainian invasion have opened a new phase. A necessary and inevitable phase of deglobalisation. It will bring manufacturing, investment and jobs back to the West. The losers will be the autocracies in the emerging countries, the large Western corporations that sell (and produce) in the emerging countries, and the large and small traders who profit greatly from the fat margins associated with imports from the emerging countries. Europe, like the US, has allocated large funds to help emerging countries, for their economic and democratic development. The opportunities for Western corporations will have to go hand in hand with the democratic development of the countries where they invest.

To open a long period of stalemate in the path of progress, like the Middle Ages. However, Covid and the Ukrainian invasion have opened a new phase. A necessary and inevitable phase of deglobalisation. It will bring manufacturing, investment and jobs back to the West. The losers will be the autocracies in the emerging countries, the large Western corporations that sell (and produce) in the emerging countries, and the large and small traders who profit greatly from the fat margins associated with imports from the emerging countries. Europe, like the US, has allocated large funds to help emerging countries, for their economic and democratic development. The opportunities for Western corporations will have to go hand in hand with the democratic development of the countries where they invest.

In November 2019, the book “Meeting Globalization’s Challenges”, a collection of pieces by distinguished economists on the topic of globalization, was published. The introduction was left to Christine Lagarde, then General Director of the IMF, one of the most influential and most criticised international institutions. It is precisely her introduction that is a sweetened re-presentation of the narrative offered in the 1990s and early 2000s about the goodness of globalisation. There are several references to papers of dubious quality and transparency showing that globalisation does not lead to job losses in the West. More transparent, however, but highly questionable, is the description of how re-training and social safety nets would protect the weakest in the West from globalisation. While admitting several errors, Lagarde, inevitably, still in 2019 defended the IMF position, written by the US years under the dictation of big corporations, the primary beneficiaries of globalisation. We know that propaganda does not only exist in Russia.

It is precisely her introduction that is a sweetened re-presentation of the narrative offered in the 1990s and early 2000s about the goodness of globalisation. There are several references to papers of dubious quality and transparency showing that globalisation does not lead to job losses in the West. More transparent, however, but highly questionable, is the description of how re-training and social safety nets would protect the weakest in the West from globalisation. While admitting several errors, Lagarde, inevitably, still in 2019 defended the IMF position, written by the US years under the dictation of big corporations, the primary beneficiaries of globalisation. We know that propaganda does not only exist in Russia.

One of the pieces in the book belongs to Nobel laureate Paul Krugman, one of the exponents of sustainable capitalism. Here the economist acknowledges his mistake when, in the 1990s, he supported the process of globalisation, defending it against the accusations of those who said it would increase social inequality and impoverish the West. In fact, globalisation soon turned into what some economists dubbed ‘hyperglobalisation‘, responsible between 1998 and 2005 for the loss of 10% of the manufacturing workforce in the West, over 10 million people. This number has continued to rise until today, with damage to the social fabric of the West and its supply chain.

In fact, globalisation soon turned into what some economists dubbed ‘hyperglobalisation‘, responsible between 1998 and 2005 for the loss of 10% of the manufacturing workforce in the West, over 10 million people. This number has continued to rise until today, with damage to the social fabric of the West and its supply chain.

Political Europe today is finally united. The atrocities in Ukraine and, before that, China’s lack of transparency linked to Covid, have shaken public opinion and politics. Corporations are also realising that the pursuit of short-term profits can create major problems in the long run. Today there is total alignment. Hyperglobalisation is over and we are moving towards a path of substantial domestic investment, which will create jobs and support wage developments and purchasing power. Some corporations will suffer, but then they will regain in the West some of the growth they have lost in emerging countries. Countries like China, India and the Middle East, which have implicitly approved of the massacres and violation of sovereign territory in Ukraine, will be affected by this shift in perspective.

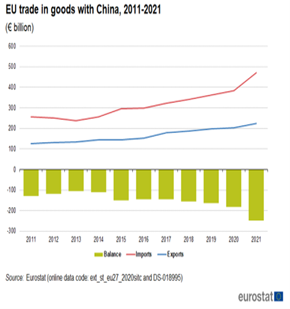

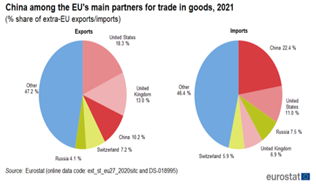

Today, Europe has a trade deficit with China of over USD 300 billion. These are not just useless teddy bears or acrylic blouses, but much of it is advanced machinery (see graph on the right). Much of this will have to be produced in the West in future.

The lights of the Renaissance now seem to prevail over the shadows of the Middle Ages. If this is the case, we can look forward to years of good growth in Europe, the reabsorption of debt accumulated during the Covid era, fiscal and political union. On the other hand, we should say goodbye to disposable T-shirts and plush toys. With significant benefits for the environment.

Optical illusions

A lot works sinusoidally. We would say everything, when there are human beings involved. The market teaches us this on a daily basis. Last weekend the hope for a ceasefire in Ukraine seemed to grow. This weekend it seems to be shrinking. Fears, albeit remote, of Russian use of tactical nuclear warheads or chemical weapons are re-emerging in the newspapers. The success of the Ukrainian army is being questioned. Putin’s determination to continue the war, as he himself stated during the recent pro-war demonstration in Moscow, seems certain. The willingness of the Chinese to support the Russians, veiled by Xi in his video call with Biden on Friday, seems dangerous.

In reality this is not the case.

Pere Borrell del Caso – Escaping Criticism, 1874. Oil on canvas. Collection Banco de España, Madrid

What we see today is a tug-of-war in view of an agreement that is just a few lines away from being signed. Putin needs to save face. Russia demands the neutrality of Ukraine (a huge step backwards from the “denazification and demilitarisation of the country”), the recognition of Crimea as part of Russia and the recognition of the two regions of Luhansk and Donetsk as independent states. Ukraine accepts neutrality, but does not recognise the expropriation of Crimea or the independence of the two republics. Moreover, expropriation by force can never be accepted as a matter of international principle. Moreover, thousands of lives would have been sacrificed for nothing. So an agreement on the independence of the Crimea (which its population would approve in a referendum, as has happened in many countries in the past) and a form of boosted autonomy for the two republics is likely. Finally, war damage. Here the tug-of-war is tight, but they will be granted against a relaxation of sanctions. We believe that Russia cannot politically afford to continue the war to the bitter end. That is why it is important to make it look like it can, to have more strength in the negotiations. Moreover, the conquest of Mariupol and thus of access to the sea from Crimea to Russia is crucial. Its return can be bargaining material at the agreement table. As for China, it does not want to weaken Putin’s position now that he is negotiating. But it certainly exerts pressure for a cessation of hostilities. China absolutely must avoid being cut off from the West, a West that already seems inclined to do so (see previous article). The confirmed news that China has denied spare parts for aircraft to Russia goes in this direction. The market relief offered on Thursday by the Chinese government expresses strong unease and growing concern.

We cannot say how long it will take but we believe a ceasefire is close. And the last days before the ceasefire will be the days when Russian forces launch their last and fiercest attack. This phase has already begun.

Putin will save face. He will probably sell the war damage to be paid as aid for the friendly country devastated by Nato pressure. However, gradually the truth will come out. In the meantime the Russian population will be dramatically affected, even though many of the sanctions will be lifted in the coming months. This could lead within a couple of years to Putin’s departure, not unlike the departure in 1999 of Boris Yeltsin. A departure apparently voluntary, but in reality obligatory. This should mark the beginning of recovery for this huge country and its unfortunate population, which has not benefited from global growth for the past 25 years. The graph opposite shows the GDP growth of China and Russia over this period.

Putin will save face. He will probably sell the war damage to be paid as aid for the friendly country devastated by Nato pressure. However, gradually the truth will come out. In the meantime the Russian population will be dramatically affected, even though many of the sanctions will be lifted in the coming months. This could lead within a couple of years to Putin’s departure, not unlike the departure in 1999 of Boris Yeltsin. A departure apparently voluntary, but in reality obligatory. This should mark the beginning of recovery for this huge country and its unfortunate population, which has not benefited from global growth for the past 25 years. The graph opposite shows the GDP growth of China and Russia over this period.

As for the recession that many expect, we believe it is very unlikely. If you watch TV you can see the damage to the economy in European countries. The media creates a lot of anxiety. This damages aggregate demand. However, we can’t help but notice how the removal of covid restrictions leads people to go out and spend. Spring has started and this trend will increase. Temperatures are rising and the price of natural gas will fall. Oil supply remains plentiful, its price reflecting speculation. Finally, in the wake of this anxiety, which also grips institutions as always, new fiscal policies will be implemented and will manifest their benefits well after the end of the war. The only (apparently) positive thing circulating is that ECB rates will not rise. Here too we disagree. Rates will go up soon, fortunately.

Ultimately, we believe that any downturn in the market can be a good opportunity to increase exposure to equity, particularly the value component, which is the most affected in this phase as it is generally more linked to economic growth. This is always within the framework of a balanced allocation, which takes due account of the risk profile of the product/investor and respects diversification, which must always be significant.

Back