“S’ha da aspettà, Ama’. Ha da passà ‘a nuttata”

Download Pdf

In these last few days, the desire to stay invested in equities is understandably being put to the test.

As we know, there are many problems, but let us try to put them in perspective together with the opportunities that tend to be forgotten at these junctures.

-

Rates go up. Rising rates take liquidity off the table and therefore less leverage and less investment. However, more ‘normal’ rates help the profitability of the financial system, reduce corporate and public pension deficits and increase savers’ returns. In addition, rate normalisation reduces speculation, the enemy of long-term real growth. As for mortgages and the real estate market, let us remember that a family buys a house when it is confident about the future of its job, and a 2 per cent higher interest payment is only decisive for the highly leveraged real estate company.

-

Inflation is very high, not far from 10%, in both the US and Europe. However, 1/3 of that in the US and 2/3 of that in Europe derive from the volatile components related to food and oil, now under pressure as a result of the war. Once the war is over, the rate should gradually fall to levels close to, but above, 2%. However, this inflation wave is important to stimulate the economy in areas like Japan and Europe, which have been locked in a deflationary grip for years. While it is true that inflation initially weighs on the consumer, it is also true that it then reactivates the wage dynamic, stimulates the real estate market, particularly in secondary areas, and makes listed companies linked to the real economy, with plants and assets, even more attractive, those that are now on the value side. While it is true that some sectors may initially suffer in terms of profits, it is also true that in the medium term almost all companies post higher profits in an inflationary environment, at least nominally. Finally, inflation reduces public and private debts.

-

High oil, gas and agricultural commodities represent a tax on the consumer. However, they also represent a huge incentive to invest heavily in energy and food, sectors that are crucial not only from an environmental and social point of view, but also because they are highly capital intensive. Agriculture means fertilisers, seed, farm machinery and land that gains value. Energy means renewables, grids, pipelines, hydrogen, as well as stimulating the growth of gas supply through more upstream investments. We are talking about hundreds of billions of dollars of increased investment over the next three to five years as a result of the anomalies that emerged with the war. This creates a powerful flywheel that feeds aggregate demand.

-

War is a dramatic event. Not a day goes by without our thoughts going to the families devastated by the conflict. However, wars end. And this one will be no exception. The longer the war lasts, the more volatile the markets will be, but the greater the likelihood that Putin’s regime will end. A long war will be difficult to explain even for a totalitarian regime. Once it is over there will be hundreds of billions of euros to spend on rebuilding Ukraine. Europe will finance a large part of the reconstruction and benefit proportionally.

-

So much we complain about supply chain bottlenecks, but little is said about the fact that these are an integral part of the deglobalisation process that will bring so many important manufacturing processes back in-house, supporting the already strong labour market.

-

The announced global fiscal stimulus has yet to be released to a large extent and will support the above trends, particularly in Europe, Japan and Korea.

-

The ECB has disappointed to some extent. True. Having already prepared an instrument against another eurozone crisis (‘fragmentation’) would have been wise. It probably takes some tension in the markets for it to be prepared, otherwise there is a lack of political support in the Netherlands or Germany. Today, however, another eurozone crisis is highly unlikely as it is known that in that case the ECB would certainly intervene clearly and quickly, with instruments that are already known and effective.

-

Even in the event of a technical recession, it is better not to bet on sharply downwardly revised profits. The dynamics described, in addition to the desire to restart after the pandemic, and the over-savings accumulated during it by households, will act as an impulse for consumption.

- Valuations on the traditional side are very low, particularly outside the US.

Against a backdrop of war, inflation, the end of QE, tech bubble deflation and with a likely tech recession in the US coming, it may seem easy to bet against the market and follow the trend these days. We wouldn’t. If these themes keep the market capped for now, the above arguments create important support for it. It will continue sideways and this will give the most flexible people a chance to buy on weakness (not tech) and release on strength. We should probably wait for the technical recession in the US with the inevitable inflationary slowdown to lift the stops and enjoy a significant market rerating, starting with Europe and Japan. Since the downside of the market today is limited (traditional/value side) we believe it is better to stay there and take advantage of these stressful phases to accumulate financially sound stocks with a good franchise and low or very low valuations. And you are spoilt for choice….

Panta rei

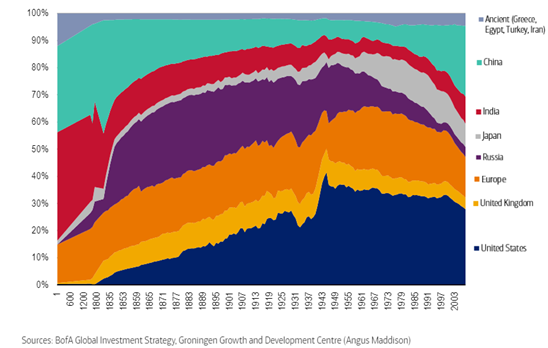

A couple of weeks ago Bank of America published a report by Peter Harnet in which a very interesting graph appeared. It illustrates the breakdown of global GDP by geographical area in different historical periods. So you can see that 2000 years ago China, India, Greece, Egypt and Turkey accounted for 84% of global GDP. In the mid-1800s Russia and China accounted for about 40%. Communism reduced them greatly. In particular, Russia went from 30% in 1800 to its current irrelevance, probably made even more extreme by the recent conflict. While China returned to growth with the advent of Deng Xiaoping’s ‘market socialism’, rising from 5% in the 1970s to 25% today. The growth following its inclusion in the WTO in 2001, which marked the beginning of the extreme phase of globalisation, was dramatic and coincided with the reduction in weight of Western countries. Japan grew from nothing to 5% with the economic expansion of the Meji era (1868-1912) that ended the shogunate and samurai rule. The Second World War heavily downsized Japan, which then, however, from 1960 to 1990, rode two phases of exceptional growth that brought it up to 14% of global GDP. Almost 30 years of deflation and bear market then brought it back to 6%, and now there are signs of stabilisation. Britain experienced its heyday in the Victorian period and has always declined from there, although less than Europe. The next few years will see the results of Brexit on the country. Europe managed to stay relevant for 2000 years, with relays between the Romans the French and the Germans. The peak was reached in the 1960s and 1970s with the creation of what would become the European Union. Unfortunately, there was then a gradual decline that accelerated dramatically with China’s entry into the WTO. After that phase, Europe lost about 10% of global GDP. India has also remained relevant over time. After the glories of 2,000 years ago, when its GDP was larger than China’s and touched almost 40% of the global GDP, there was a gradual decline in importance that became more pronounced with the departure of the British and the partition of the country. A country with great resources but a confusing democracy, India remained at around 5% of global GDP throughout the 20th century and is now showing signs of revival, unfortunately, as is often the case, with a democracy with autocratic overtones. Finally, the United States. They are those among the Western countries that have been best able to manage globalisation, limiting their loss of weight, which nevertheless amounts to 5% since 2001.

Everyone can draw their own conclusions. We limit ourselves to a few reflections.

An autocratic government that does the right things can often accelerate the country’s growth, but if it does not, it can easily be the cause of the country’s demise. So for investment, a democracy, however imperfect, is always preferable.

While recognising the merits of globalisation, it was badly set up and led to an adjustment too fast. The results are there for all to see, with a West dependent on a powerful, autocratic, belligerent China with completely different values from the West.

Russia seems ready to hit rock bottom and we would not be surprised if this mad war represented the final stage of its dramatic decline.

Europe could probably find in a true union the solution to get out of the decadence in which it finds itself. While it is still difficult to be optimistic on this front, we can say that we are more so than we were three years ago.

Global GDP breakdown by geographical region over the past 2000 years

Back

acarbose alcohol

acarbose alcohol