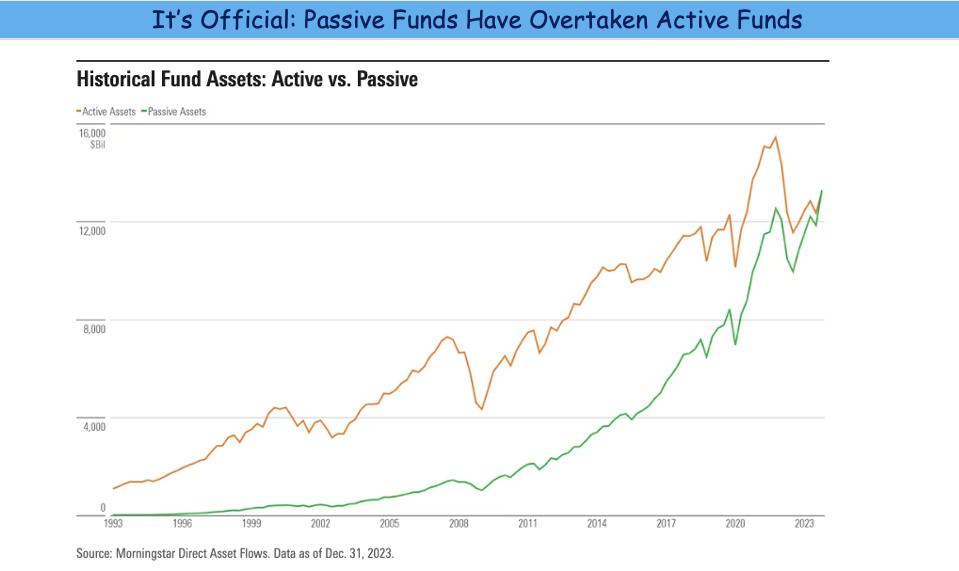

Has passive investment broken value investing, as argued by Greenlight Capital’s Einhorn? See here.

The logic is clear. By throwing in a wall of money onto stocks, or withdrawing that wall, no matter the valuation or fundamental strength of the underlying company, index investing undermines the signalling function of market prices for the allocation of capital and along with that the efficacy of value investing.

Passive investors – Einhorn’s argument goes on – have no opinion about value, which means that “when money is moved from active to passive, value managers get redeemed, value stocks

go down, it causes more redemptions of value managers, it causes those stocks to go down more and so on”. The conclusion sounds somewhat apocalyptic: “the value industry has gotten completely annihilated”.

There is certainly some truth in this argument, but paraphrasing Mark Twain, reports of our death are greatly exaggerated.

Passive investing in the US, the world’s biggest market, is (for now) only ~50% of institutional equity funds, which means that the remaining US$14.3 trillion of active investing is reasonably

more than enough for the price discovery mechanism to continue functioning. In fact, just a small share of fundamental, active investing would probably do the job.

In general, there is ample evidence that passive and active value strategies complement each other, with passive being often the core of a portfolio and active value a portion allocated for

potential outperformance, thematic exposure and risk mitigation. Today, value investing provides a much-needed counterbalance to passive investing and to investor euphoria about technology stocks.

This is a marketing communication for institutional investors. Please refer to Fund Prospectuses & KIDs before making any investment decision.

For any questions email us on: info@nicheam.com

Follow us on LinkedIn: www.linkedin.com/company/niche-am

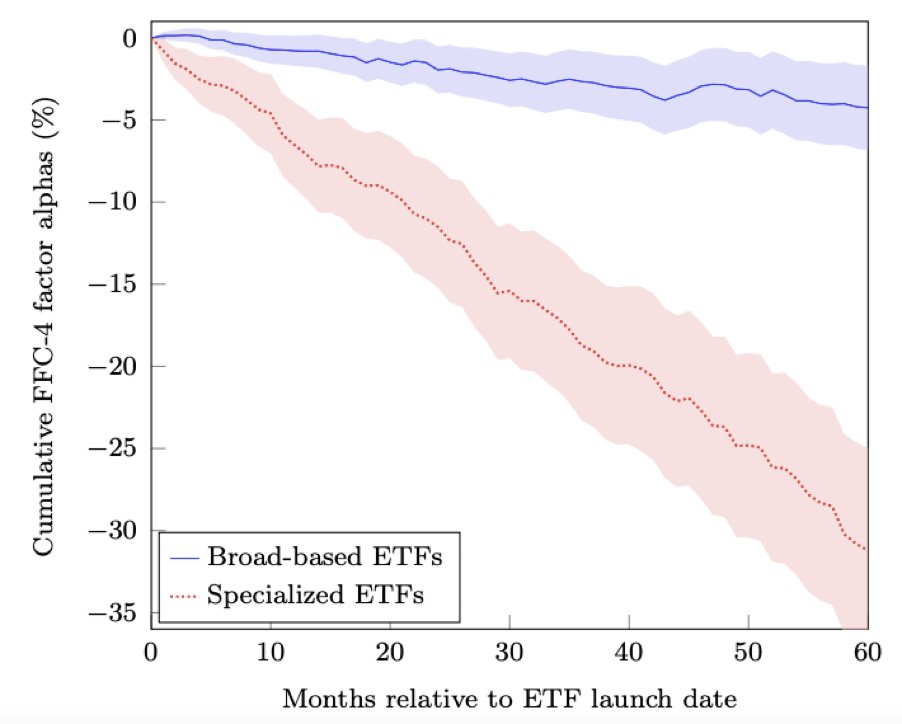

Read MoreDoes thematic investing create value for investors?

Not quite, according to this NBER paper which shows that at least in the ETF space, thematic investments underperform broader funds by about a third over the five years after launch, delivering negative alpha of about -4% a year.

The argument is not new: thematic ETFs are generally launched just after the very peak of excitement around an investment theme, holding portfolios of “hot” assets already overvalued at

launch and with über-high expectations. As industry and media hype vanish or financials disappoint, thematic investment underperforms or delivers negative risk-adjusted returns.

We couldn’t agree more.

That’s why at Niche AM we don’t really invest in themes but rather in niches, i.e. assets or themes which are all but neglected by the market and are thus deeply undervalued and entirely off-radar for investors and media.

Niche AM’s mission is somehow to find a theme before it becomes so. The niche may take time to attract investors and deliver potentially strong returns, but the enormous valuation opportunity makes it worth the wait.

This is a marketing communication for institutional investors. Please refer to Fund Prospectuses & KIDs before making any investment decision.

For any questions email us on: info@nicheam.com

Follow us on LinkedIn: www.linkedin.com/company/niche-am

Back Read More

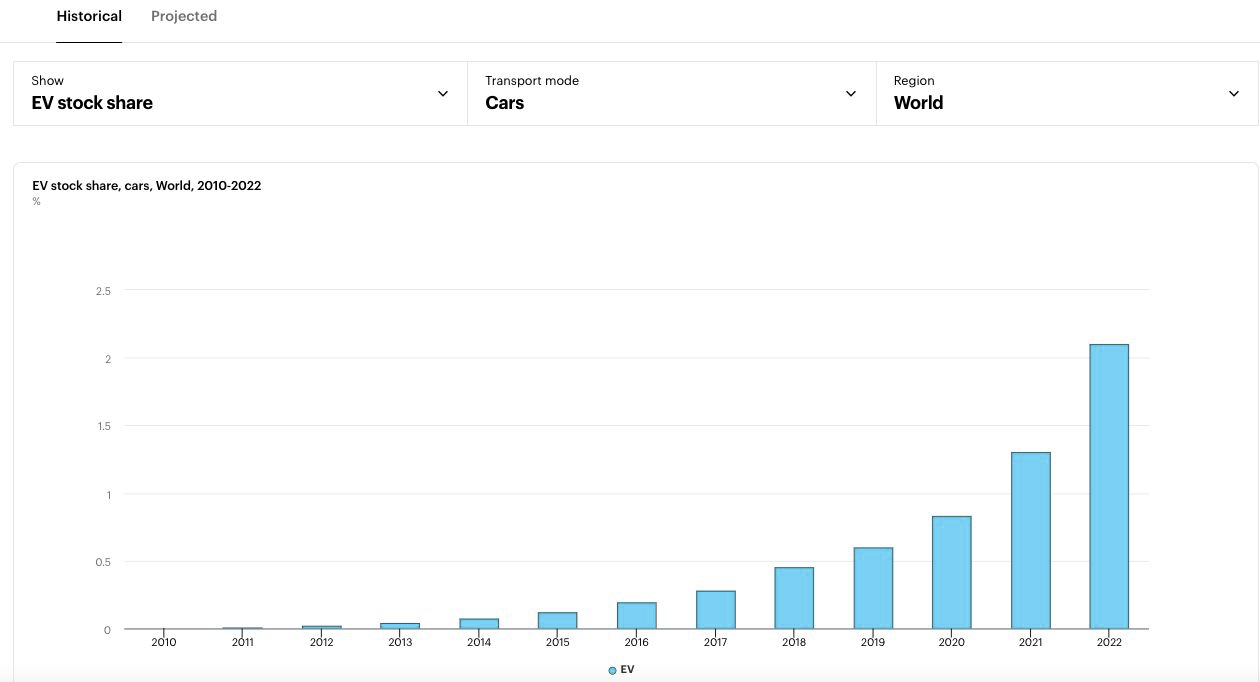

Electric mobility funds have fared poorly since the middle of last year mainly on concerns about China flooding the market with cheap EVs, with some ETFs declining by as much as 30%-35% since July.

This looks overdone, partly the result of the pendulum in investor sentiment between euphoria and pessimism.

The future of the world remains squarely electric, with the electric mobility megatrend here to stay, supported by environmental concerns, government incentives, technological progress (making EVs more affordable and better performing), infrastructure development and favourable consumer preferences.

Global market-sales share for electric vehicles is growing fast but remains at an average of ~15%, while global market-penetration is still on average ~2.0% (source: IEA).

In other words, e-mobility has not even embarked on the fast-growth and fast-adoption stage of the S-shaped penetration curve but some investors have seemingly already given up.

Paraphrasing MIT’s Malone, every technology breakthrough takes twice long as expected but half as long as the industry and the market are prepared for. And what the market is not yet prepared for and therefore not yet pricing in e-mobility stocks is the under-capacity scenario we still expect for the battery space, which should give key battery players stronger pricing power, better margins/earnings and higher valuations.

Yet not all that shines is gold….and not all e-mobility funds are equally attractive or equally effective in generating returns while protecting capital across cycles.

Our Electric Mobility Value Niche is a global equity fund that offers exposure to the EV battery ecosystem, investing in electric mobility players not recognized as such by the market and thus with potential for significant re-rating. The battery ecosystem represents 75% of the portfolio.

The chart below shows performance since inception for Niche AM’s E-mobility Value Niche fund vs ETF peers BATT and LIT. Yes, the latter has generated slightly higher returns over the period, but it has achieved so with double the volatility and a drawdown 3.5x as high.

At Niche AM we believe investment is as much about generating returns as about controlling risk, which we do by:

1. adopting a deep-value approach, as the price paid for the asset is the main determinant of its downside risk – this approach eliminates the risk of investing into a bubble

2. avoiding leverage at companies held in the portfolio

3. building a highly diversified portfolio

4. implementing an ESG-responsible approach, which reduces regulatory and political risk.

Within this framework market-timing, always challenging if not impossible, becomes less warranted.

For details on our EMVN fund see here.

This is a marketing communication for institutional investors. Please refer to Fund Prospectuses & KIDs before making any investment decision.

For any questions email us on: info@nicheam.com

Follow us on LinkedIn: www.linkedin.com/company/niche-am

Back Read More

Will value stocks outperform growth in 2024? No one can know. Paraphrasing Galbraith, the only function of market forecasts is to make astrology look respectable.

Stock prices are the result of the aggregated activity or decisions of billions of producers, consumers, workers, investors and savers across the world influenced by forces which are sometimes known in advance but most often unknown and random.

Within a time-horizon as short as 12 months anything could happen and market-timing stocks or investment styles would just be speculation, not investing. Diversification and a well-balanced portfolio of both value and growth stocks remain the best long-term strategy for investors.

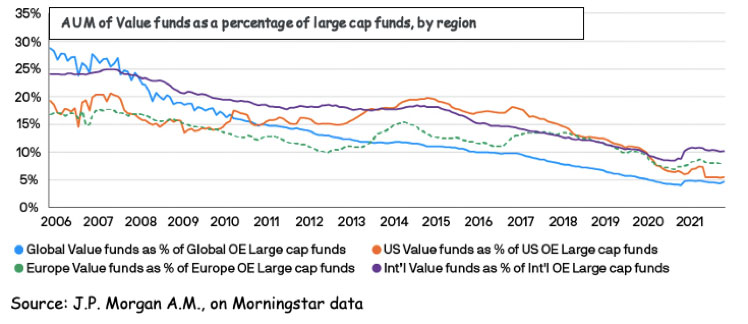

That said, what is the investment case for a rotation out of growth into value stocks? There are several drivers, some of which the result of possibly new structural trends.

Both investor positioning and valuation spreads are too extreme.Partly forced upon investors by the composition of major stock indices, the proportion of value funds over total equity funds has fallen to as low as 5%-10% from the 20%-25% of the years before the Great Financial Crisis. Valuation spreads between value and growth stocks remain near historical highs, even higher than at the zenith of the TMT bubble. This look unsustainable if mean reversion is to maintain a minimum of credibility as investment tool, or even only for diversification and risk mitigation.

Back Read More

As the Nikkei 225 continues to hit new highs, the question for many investors seems to be: is this it, is the rally done?

We think Japan’s equity market remains a trove of quality, competitive, high-earning and undervalued companies, which is now benefitting from an accelerating wave of reforms in corporate governance and financial regulation.

Despite the recent rally, Japanese equities remain below 1989 levels. Market valuations are still attractive: ~1/3 of listed companies have 40% more cash than their market capitalisation while ~45% trade at less than 1x tangible net assets and ~60% are debt-free.

Recent updates to the corporate governance code, which pressure listed companies to offload their large equity cross-holdings, could result in ever increasing M&A and MBO activity as controlling shareholders try to fend off the risk of shareholder activism.

Further support could come from the ripple effects of the introduction last year of the Tokyo Stock Exchange’s 1x Price-to-Book rule, which requests listed companies trading below book value to explain their action plans to generate returns above the cost of capital and close the valuation gap. This should help drive greater management focus on shareholder value and further accelerate the pace of buybacks.

Retail inflows into equities could also increase after last year’s revision to Japan’s tax-free individual investment accounts, which is aimed at freeing ~€12.6 trillion in household financial assets mostly held in cash deposits.

Geopolitics should also help: Japan is increasingly seen as a play on China’s possible economic recovery without its geopolitical and domestic policy risks.

An uncontrolled Yen appreciation as a result of higher interest rates could have an impact on Japan’s equity market (mainly via negative effects on exporters) but it is also conceivable that at least a part of the funds which would repatriate following the break of the carry trade could find their way into domestic equities.

By focusing on companies not covered by the sell-side, our Orphan Companies project invests in a market niche which is even more undervalued than the wider Japanese mkt, offering thus investors a further margin of safety.

Sell-side coverage is often essential to attract investors and boost valuations but coverage can be expensive and time demanding and after 30 years of challenging markets many brokers have cut the number of companies under coverage.

As a result these companies trade a huge discount versus their peers, a discount which normally closes at initiation of broker coverage (or in the event of corporate action).

These are deep value opportunities: the 168 small and micro cap companies in our Orphan Companies portfolio trade an average PE of about 9x, a price to tangible book-value of about 0.6x and a net cash to market-cap ratio above 120%.

For further details see our Japanese Orphan Companies Project presentations.

For any questions email us on: info@nicheam.com

Follow us on LinkedIn: www.linkedin.com/company/niche-am

Back Read More

The amount of negative press about ESG may be a sign that we are nearing the peak of the current backlash against ESG investing. Will the peak in negative sentiment be reached around Donald Trump’s possible re-election in November?

Everybody seems to be ranting against ESG these days. Some posit that the excessive number, complexity and sometimes vagueness and inconsistency of the UN’s SDGs make of these just a sort of humanity’s wish list, a mere list of desirables which is not accompanied by a realistic and effective strategy.

While they might have a point, it is just another sign of the current shift of the pendulum against ESG not only in media but also in politics and financial markets.

Investors who until very recently were happy to pay irrationally high multiples for ESG assets are now treating these as kryptonite even at ultra-low valuations.

Not us. We don’t see ESG investing as a transitory fad but as a structural and long-term mega-trend which is here to stay. All our investment portfolios are SDG-focussed, mostly as a way to minimise regulatory risk and ensure long-term profit growth. But also to maximise long-term investment performance.

Much of the recent scepticism around ESG performance is caused by the swinging fortunes of the energy sector. In fact, when controlling for sectoral effects (and also for investment style such as value and growth) it seems that ESG factors do continue to ensure outperformance, as nicely showed in the chart.

Back from vacation. The heat, while acceptable on the beach, is unbearable in town. The market is boring, weak, doomed. Good news is bad news. Bad news is, well, bad news. Good companies reporting bring a few percentage points of gain to the poor investor. Disappointment brings double digit losses. Why stick around? Why not sell and go back on beach?

Valuations?

There is a great deal of confusion in the market right now and many investors are still sceptical. They mention valuations, interest rates and economic slowdown as their primary concerns.

On valuations, we can say we have rarely in 25 years of tenure as fund managers experienced valuations that are so depressed. The indices apparently look expensive based on historical data. Those data do not take into consideration that today, in particular in the US, we have a significant amount of growth stocks in those indices. So, we would not rely on dumb averages. The stocks in the traditional sectors are, in many cases, very attractive. If we look at the risk premia, we also note that the actual ten-year interest rates cannot be considered a reference point due to its volatility. Common sense tells us that we should take an average of the last few years. Then, we have long term trends like energy transition and business onshoring that should support and energize the economy in the next few years. Last but not least, the inflation of the past three years has still to be fully reflected in the EPS.

If you take into account the previous elements, indexes composition, free risk, long term trends and laggard inflation effect on EPS, valuations are at their most attractive.

We think that once the economy presents its first signs of recession, unavoidable under the pressure of high interest rates, and the doomsayers start calling the stagflation myth, the traditional part of the market, the one that is now in value/deep-value territory, will gradually start to roar back, anticipating the inversion of the interest rates cycle. This is when retailers, consumer stocks, housing related stocks, leveraged companies, banks, etc, somewhat counterintuitively, will start to bounce back from shameful levels.

We are getting close to that moment. Today we think it is a perfect time to gradually accumulate deep value stocks. This part of the market includes thousands of quality names worldwide, very often far from the radar of investors who generally focus on about 5% of the total listed companies worldwide. It is now the time when “you can buy scores of decent companies at amazing prices”, quoting Warren Buffet.

What are we looking at these days?

The recent investment lull among the main telecom operators in North America has weakened the telecom equipment sector despite a global competitive outlook that has much improved. Here we find many companies we like.

We are also trying to time the end of the streaming war, tiptoeing into late comers, names like Paramount in the US, and RTL in Europe and others. These are companies with great content franchises. In one of our two multi thematic funds we also have a niche dedicated to publishers, a devasted sector where we see great revival potential. Bombarded by lots of fake news, democracies need to rely on serious journalism. The few survivors will thrive.

Renewables are again under pressure. What an opportunity! As we see Russia, the Middle East and China coordinating to support the oil price, pollution increasing and global warming producing the worth heatwaves to date, the market is again dumping the renewables players. The reason? There is a tug of war between the renewable energy supply chain and the utilities. The former wants significant price increases. The latter resists. It is normal. But the former will win in the end. We must take advantage of this phase. Buy the main players that present solid financial positions and clear undervaluation. We have an oversized position in Siemens Energy that is giving us some headaches, but we are happy to increase it on the way down. We are also adding to other renewable holdings, and we are introducing new ones in the US, Europe, Japan and South Korea.

In this phase of economic slowdown, we are also increasing on weakness stocks related to transportation, mostly in Europe where they are cheaper. We are also courting the timber sector, down with the cycle, but ready for a powerful rerating, forest owners in first place.

Companies in the sectors mentioned must be cautiously handled, some having significant financial and/or operational leverage and being now out of consensus. That’s why diversification is important. However, those and many other companies now present a great risk/benefit profile, the only metrics we use to appraise companies and build portfolios.

Our process

We define a strategy before investing. This strategy must clearly be flexible enough to be adjusted, but we tend not to be distracted by the news flow. We value the companies by what we see now, in terms of earnings potential (normalized) and assets held.

We do not speculate about long-term opportunities. If the companies are not deep value anymore, we take profit. Very rarely, we sell before our strategy plays out. Often, when all, according to the news flow, looks lost, something comes to the rescue. Before buying we want to see a huge discount, we are careful of debt, and we LOVE diversification (even if it has never been so unfashionable in the industry). Our funds proudly hold hundreds of stocks. This approach limits the impact of the black swans.

We buy gradually on the way down; we sell gradually on the way up. When we start to buy, normally the stock in the short term continues to go down. When we sell, the opposite happens. Sometimes we take partial profits before our target is reached if we see opportunities to further diversify our portfolios with stocks with a good risk/reward profile.

We are now very optimistic about the markets we follow. As mentioned above, there is such an abundance of quality stocks in the deep value camp. The market looks tired. The negatives apparently outnumber the positives. This makes the odds of a dramatic rebound in the many deep value stocks available even more likely.

As mentioned, the economy is also currently supported by robust geographical long-term trends. Europe and Japan could be coming out of stagnation. The China-driven world deflation pressures look to be gone. US economic drivers remain robust. Korea, Indonesia and a number of other countries can be seen as manufacturing alternative to China.

Central banks are weakening the economy to break inflation’s back. However, central banks can be very fast to reflate the economy if it weakens too much. Again, once inflation is tamed (and the market always tries to anticipate this) we expect a violent rerating of this part of the market.

We don’t know what will happen in the next few months but, again, we think the downside on our universe is limited, the upside huge. Here we see an opportunity. Be patient. Quit the screen, buy a few books, travel, relax. It is incredible how laziness can be rewarding in stock markets…

Read More

What is Siemens Energy?

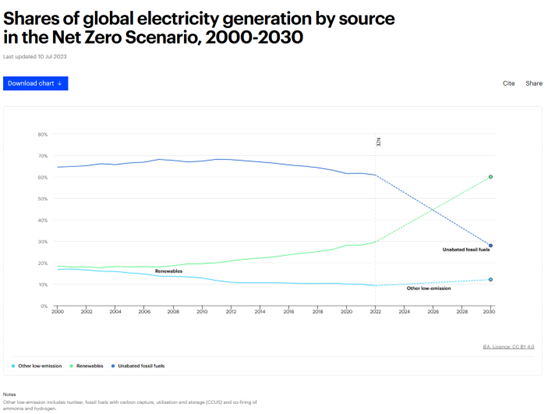

Siemens Energy is a beautiful multinational listed in Germany. It is a spin-off from Siemens in 2020. It contains two macro-businesses. The first brings together activities related to the energy grid, turbines and hydrogen. The second is a leader in the production and operation of windmills for wind energy production. We are in the era of the energy transition, where trillions of dollars will be spent to reduce poisonous CO2 emissions by investing in renewables and modernising the energy grid and infrastructure. Today, the world has about 8 Terawatts of electricity generation capacity, which is set to grow significantly with the development of electric mobility. To meet the NET ZERO EMISSION scenario to be reached in 2050, the share of electricity generation from renewables and other low-emission sources will have to increase from 37% to 73% by 2030 (see chart below).

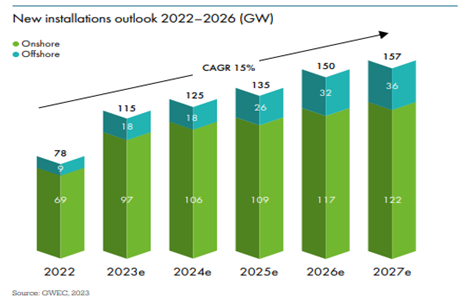

It took 33 years to reach one Terawatt (1000 Giga) of wind power capacity. According to GWEC (Global Wind Energy Council – GWEC-2023_interactive.pdf) this capacity will be doubled in the next 7 years (below is a histogram showing the expected growth in wind power capacity). Apparently, there is no better place to be invested to benefit from Siemens Energy’s energy transition trend. Apparently.

What happened?

As mentioned earlier, the company can be divided into two major divisions, one instrumental in the efficiency enhancement of existing power generation and transmission facilities, and the other focused on the production, installation and operation of the windmills that we see more and more around us when we leave our cities. The first division is emerging from a twenty-year torpor characterised by over-competition and under-investment. This resurgence is due to industry consolidation, limited Chinese competition in such a strategic sector, and the political will to drastically limit greenhouse gas emissions, which implies huge investments for the next decade.

By contrast, the second division, whose name is Siemens Gamesa, is going through a difficult phase due to its complex and relatively new nature. The construction of these wind farms consisting of hundreds of huge mills is an exercise of cyclopean proportions. To give the reader a point of reference, an offshore (shallow waters) wind farm with a capacity of one gigawatt (i.e. 1000 megawatts, the power needed to keep 100 million LED lights switched on or to supply energy to more than 500,000 households) costs around EUR 3 billion to build and around EUR 100 million per year to operate. The development of such projects extends over several years, from a minimum of 2 years up to 7 years. The organisation required is therefore very complex, not far from that needed to build a nuclear power plant and much greater than that needed to build a large dam. For the same capacity, the use of steel is 15 times higher than for a gas-fired power station. The order book for these orders extends over several years, with contracts, however, only marginally considering changes in the cost of materials. In addition, there is no compensation for site interruptions due to exceptional causes. The Pandemic and Ukrainian invasion have therefore created significant losses on these multi-year contracts. And this is only the oldest part of the story that took the share price from over EUR 30 per share to less than EUR 11 about two years ago. As is always the case, the industry then revised its price list significantly and managed to agree more favourable terms with customers that would guarantee them good future profitability. This allowed the stock to recover from EUR 11 per share to EUR 24 per share. Now comes the best part.

In May 2023, the company issued a statement in which it revised upwards its profit estimates for 2023 (the company’s statutory year ends at the end of September). The reasons lie in the first division, which sees demand and prices rising sharply. The release also mentions the second division, Siemens Gamesa, saying that progress is slower than hoped and will only be seen towards the end of the year. So, we have a division in top form and confirmation that, although slower than expected, Siemens Gamesa is recovering. Fifteen days later these elements are confirmed at the JPM conference in London (qui il link alla presentazione). In this context, even those who had exited the stock due to the disappointments associated with Siemens Gamesa gradually re-entered, pushing the share to EUR 24, a new high for the period. At that valuation, the company was still very attractive even for those of us who are ‘deep value’, i.e. we invest for what we see today, not what might be in the future. In fact, at that price, the company had a capitalisation of around EUR 19 billion. Valuing the first division at a humble earnings multiple of 11x and adding the Indian JV at market values we arrive at about 17 billion euros. The implied valuation for Siemens Gamesa was thus 2 billion, or less than 0.2X EV/Sales, one-sixth of what the company recently paid to take it off the market (4 billion for one-third of the company, so 12 billion euros) and one-eighth of the EV/Sales multiple of rival Vestas (EV/Sales 1.6X). Assuming stable sales and a return to an EBIT margin of 10% Siemens Gamesa is conservatively worth at least €12 billion (1.2X EV/Sales, 11X EV/EBIT), thus €10 billion more than it was valued at when it was worth €24, or €36 per share. Clearly the EBIT margin of 10% was not around the corner, but it was an achievable result.

On 21 June, the company came out with an explosive statement: the Siemens Gamesa division found new component and/or design problems on about 1/3 of the installed base. This will result in over 1 billion costs spread over 5 years and delay the turnaround. The company reaffirms the recently released sales and profitability targets on the first division. It withdraws the targets as a group, as it cannot yet quantify the unexpected costs on Siemens Gamesa. The share price will lose about 40 per cent of its capitalisation, EUR 8 billion, over the next two days. A large part of this fall is due to the fact that investors who entered after the recent increase in earnings estimates have exited, regardless of price, and that a number of investors who were already there have reduced their positions or not increased them by virtue of the confusion that seems to reign within the company, where problems of an extremely significant magnitude emerge from one day to the next, with top management seemingly completely uninvolved in the company’s performance.

Kitchen sinking?

Kitchen Sinking refers in finance to the attitude of providing more negative information than one already has about the company one is managing. While this immediately implies a negative effect, it also ‘skews’ expectations, improving the perception of future data. This is often done by new managers in order to take credit for future improvement. With the acquisition of the 33 per cent of Siemens Gamesa not held by Siemens Energy, the old management of this division was replaced and the leavers were blamed for much of the responsibility for the company’s years of difficulties. It is possible that the management made this unexpected decision in order to set the tone and exaggeratedly lower expectations.

DEJA VU’?

It was the year 2006 and we were investing in EADS, the company that many years later would be renamed AIRBUS. The company had many points in common with today’s Siemens Energy: 1) engaged in the capital equipment sector with multi-year orders and sensitive technology 2) the business growth prospects were exceptionally favourable 3) the company had two divisions, one producing fat profits (the Defence division) and one in difficulty (the Civil Aircraft division) 3) the division in difficulty complained of significant technical and internal communication problems 4) the company operated in an oligopoly regime with very high barriers to entry 5) the company was defended against Chinese competition 6) the company was politically significant.

It took EADS a few years to get back on its feet, but then, gradually, the rerating came. At the end of 2009, Airbus was worth about €12 billion (as Siemens Energy is today) with €42 billion in sales (Siemens Energy’s sales expected to be €34 billion next year) and a loss of about €800 million resulting from over-costs related to the A380 and A350 projects (about €1 billion in losses related to exceptional components for Siemens Gamesa). In ten years, the Airbus share has increased tenfold. Today Airbus is one of the most heavily weighted European stocks in portfolios, perceived as high quality and certainly benefiting from Boeing’s weakness and the focus in Europe on the defence sector. However, at 16x EV/Ebit we believe it does not present a sufficiently attractive risk/benefit profile given the many risks in the sector, unlike Siemens Energy.

Conclusion

Today Siemens Energy represents the classic dead dog or ‘show me’ company, i.e. a company that will have to radically surprise us in order to gradually catch up. It will probably take time and the terrain in any case remains slippery and much can still go wrong. However, the risk/benefit profile, the metric against which we assess every investment, is outstanding. The company has no debt, has a division that is doing very well with high operating leverage, and we believe that rarely has it been possible to buy a jewel like Siemens Gamesa at these valuations. By giving a valuation of 17 billion to the first division today you can buy Siemens Gamesa at a negative value of 6 billion!!! We therefore used the recent weakness to increase our positions on this company.

Nuova nicchia sul fondo Pharus Asian Value Niche

Market context

Opportunistically we seize this phase of market confusion to add a new niche. The market continues to be worried about central banks raising rates. Central banks are worried about inflation. Persistent inflation is in the current environment both inevitable and positive. Inevitable because the deflationary effect that China has exerted for two decades, sending much of the world into stagnation, is gradually disappearing. Positive because it reflects huge investments directed towards the energy transition and the rebuilding of a more reliable supply chain. It will bring down public and private debts. It will restore some of the social equity lost in recent years. It will lay the groundwork for a rise in the value component of the market that, when it comes, will be formidable, not unlike what we saw in similar situations in 1950 and 1982. Rising rates will not stop these investments but will inevitably bring problems to areas that have adapted to a very low-rate environment. We are witnessing and will witness a general clean-up of speculation that is still strong. The victims, as always, will be those who have taken the most risk; hence, have benefited from a lot of debt or excess liquidity to seek returns in speculative investments. While much of the Private Equity and Private Debt around is of quality, there is a not insignificant part of it that will go bad. It will be understood that returns of 15%/25% per year are not always the result of shining minds, but rather of the most trivial leverage. It is easily understood that a number of these gentlemen have been exchanging assets for years in order to make the famous exits. Other areas also need to be checked, in particular that sympathetically termed ‘real assets’, a definition that slyly tends to create an inappropriate sense of comfort in the end investor. We, as free-range and unrefined individuals, keep an eye on bitcoin, which has recovered well this year. Indeed, we are convinced that the beginning of the fall in rates and the subsequent historic rally in equity (value) will follow the final collapse of cryptocurrencies, the summa maxima of a historical phase defined by unbridled globalization, global stagnation, a riot of inequality and nationalism, negative rates and speculation.

Globalization by Vsevolod Slavutych

“Deglob” Niche

Many times, we have discussed deglobalization. If globalization has been the theme of the past 20 years and having understood, it and followed it in investment choices would have helped a lot. In the next 10 years deglobalization, we believe, will have equally profound repercussions. Many sectors will be affected and that could completely overhaul, positively or negatively, their business structure. We therefore create a portfolio within the Pharus Asia Value Niche fund including companies that will benefit from these changes. The sectors are the most diverse, from companies related to the semiconductor ecosystem, ingredients for pharmaceuticals, construction, metal refining, steel, communications infrastructure, renewables and many others. Siemens Energy, which we mentioned above, is clearly one of the beneficiaries of this trend and one of the stocks in this portfolio (here is an interesting article on the subject NZIA: act now or Europe’s wind turbines will be made in China | WindEurope ).

As always, there will have to be three characteristics. In addition to being able to benefit from deglobalization, companies will have to have ‘deep value’ valuations, in line with our approach, and they will have to be sustainable in the sense that they will have to position themselves on a path of gradual improvement with respect to social, environmental and governance factors. Through direct interaction with companies, we are committed to ensuring and documenting this. The new Niche starts with a weight of 1.5 per cent and has a maximum weight of 2.5 per cent of the portfolio’s NAV. Initially it consists of 15 securities which we will gradually increase to 25.

Banking crisis? Yes, but the banking sector is very solid and after the mistakes made with Credit Suisse politicians are moving to support it.

Suddenly rising interest rates? Yes, but the raising cycle is finished or almost finished.

Inflation high? Yes, but supported by the last phase of the cycle, the blessed one of rising wages.

Stock index valuations not particularly low? Yes, but today, after a decade of a bull market in growth stocks, the indexes are awash with these rightly more expensive stocks, which then inevitably raise the average price. But you must avoid looking at the averages. Value stocks have never been more attractive.

Recession? Yes, possible, particularly in the very short term after this banking crisis. But it will be short-lived if it does arrive. It will mark the end of rate hikes. Deglobalization and energy transition will sustain the economy for several years. The numbers to be invested here are mind-boggling. A new era is opening up after twenty years of stagnation and destruction of the manufacturing fabric in the West.

Sell in May and go away? Probably not this year. We would wait for the flood of dividends that will come in May and June and, more importantly, the closure between valuations and inflation that usually starts to happen when rates stop rising. Stocks are assets that absorb inflation and protect us from it, with a certain time gap. But then the catch up is violent. See the 1950s or the 1980sfor example.

In short, it will take some patience, but we would not risk losing our seat on the equity train and would take advantage of this unexpected entry point to put more cash to work in equities. Possibly value and well diversified. Meanwhile inflation is fast eroding the value of cash.

Cash is not king. Cash is trash.

Ork sculptures at Bernd Greisinger’s Tolkien Museum in Jenins – Switzerland

Credit Suisse is dead. Long live Credit Suisse!

Credit Suisse is gone, devoured by UBS. The demise of the most prestigious Swiss bank brings sorrow, not only to the poor shareholders (and we were among them), but also to the small but prestigious European nation. This cannibalistic show has been sold purely as a bailout but a bailout it is not.

Once upon a time, there was Switzerland’s most prestigious bank, Schweizerische Kreditanstalt, aka the “Institute of Credit Suisse.” It ran happily on the grassy meadows of the cantons, helping the development of its country’s railway infrastructure and the growth of the business fabric. Over time, thanks in part to Switzerland’s – let’s say banking “reserved and neutral” policy – it could attract deposits from all over the world and grew enormously. Unlike its half-sister UBS it was not declared insolvent during the great financial crisis of 2008 and did not have to be bailed out (stocks and bonds) by the Swiss state. It grew a lot and like all big banks where there are some few thousand individuals deciding the fate of large sums, some scandals occurred (here, just for equanimity some UBS scandals: notes 17 full-report-ubs-group-ag-and-ubs-ag-consolidated-2022-en.pdf. , UBS: Corporate Rap Sheet | Corporate Research Project (corp-research.org)).

A lot has been said about “tuna bonds,” bonds issued in… Mozambique, to help develop the tuna industry. Although it all took place on the “well-regulated” African continent some bribes were paid. There has been talk of the stalking related to the “poaching” of a big CS poppy by UBS to check compliance with contractual clauses. There was much talk about the managements related to bonds issued by Greensill, a company that fell into disgrace but whose endorsement politicians and opinion leaders in the UK and Australia disputed for years. They talked about the much money lost by Credit Suisse from the Archegos bankruptcy of which CS was prime broker like all the other big investment banks. CS lost much more than the others, and for that it had to make a painful capital increase that, together with the annual profit, covered the loss. An unfortunate event but far from a scandal. CS then had to fire the prestigious Horta-Hosorio, former CEO of Lloyds Bank, who had just been hired as Chair, because of his non-compliance with Covid rules. Again, hard to see any negatives here. If anything, the opposite. Axel Lehmann was then hired in his place, by someone who was certainly not superstitious…

Over the past five years, CS’s goal was to gradually reduce size and risk and move toward a business model closer to Julius Baer, which trades at 3x tangible net worth, rather than UBS, which before the acquisition traded at 1x. Credit Suisse at the start of the year traded at a fraction of what UBS traded at. To confirm the strategy, we point out that Credit Suisse reduced assets by almost 40 percent from 2020 to 2022, from about CHF 819 billion to CHF 515 billion. When big asset reductions happen, it’s normal for profits to fall, at least initially, and for some extraordinary costs to be recorded.

In the past two years it’s been touching how several newspapers and websites have looked after CS. The Inside Paradeplatz blog and the FT have been among those at the forefront of this initiative, to mention the most prestigious. Every day an article. In some case a light negative insight and, in another, a saber-rattling a frontal attack on the bank’s stability.  This even though the bank was apparently a solid global financial institution. However, family offices, funds and rich people who read daily negative press about the institution where they store their cash, may have been asking themselves questions. A frontal press attack, devoid of substance, occurred in October, right during the company’s black period. This led to an initial bank run that culminated in a capital increase that, on paper, was not needed. Arab investors increased their positions, and the bank decided to accelerate its transition to a low-risk reality.

This even though the bank was apparently a solid global financial institution. However, family offices, funds and rich people who read daily negative press about the institution where they store their cash, may have been asking themselves questions. A frontal press attack, devoid of substance, occurred in October, right during the company’s black period. This led to an initial bank run that culminated in a capital increase that, on paper, was not needed. Arab investors increased their positions, and the bank decided to accelerate its transition to a low-risk reality.

However, the press did not let up. Even the auditor’s recent recommendation to strengthen the company’s account controls, not unusual for an auditor, was presented almost as an effort to falsify the accounts, although the accounts were in no way corrected. Patrick Jenkins, deputy editor of the FT, came out with an aggressive article on Feb. 23 (Six numbers that show why Credit Suisse has little leeway | Financial Times (ft.com))[1] in which he inexplicably painted every item related to this bank in black. The U.S. banking crisis then came unexpectedly, unfortunately infecting the industry in Europe and hitting the most talked-about player (certainly not the weakest).

What is a state supposed to do when a player that is solid on all the metrics by which regulators measure banks turns out, in the context of a global financial crisis, to be the subject of noise culminating in a bank run? Probably stand behind the institution with all its power, setting a precedent for the speculators. Certainly not what the Swiss State did. It is possible that regulators and politicians were skillfully directed during this panic phase by the predatory instinct of UBS management, and they created a disaster.

The bottom line is that no matter how sound a bank is, if it is the victim of a bank run it must be shut down and shareholders and AT1 bondholders could lose everything or almost everything. So, what metrics can an equity or a bond manager evaluate a bank with? How much capital and liquidity must a bank have in such an environment? And thus, when can this ever pay back the cost of capital? Alternatively, to protect against bank runs, the regulations must be changed, and the deposits completely protected. But how does the banking system or even the state guarantee all the deposits? Another alternative is that liquidity must be hugely increased (CS had a top liquidity ratio, above 150%, four days before its fall) but then lending will have to be much lower, with huge repercussions on the money multiplier and thus on the economy. In short, the Swiss authorities’ mess will have to involve new regulations and guarantees. In the meantime, we advise banks to spend lots of money on their IR function, buy lots of adverts in newspapers, invest in freemasonry and political lobbying, keep the best journalists close and constantly well informed. In short, make sure to have some form of control on the news flow that could lead to a ban run, to the benefit of everyone, from investors to depositors and consumers. Credit Suisse did very poorly on this side.

In all this, what did UBS managers do? Cunningly pushed politicians and regulators to give them CS at a negative value of CHF 14 billion (it paid 3 billion CHF in shares for 57 billion CHF of tangible equity, let alone the goodwill), probably waving the sword of Damocles over the fall of the system and thereby fulfilling their mandate to create shareholders value (in this case the shareholders’ value created has been epic!). While UBS management and current shareholders of UBS benefit a great deal from this, in the long run it will bring it some negatives too. UBS will remain in the imagination of the educated Swiss as a global bank that used its strength to weaken the country it represents, the country that saved it in 2008 from certain death, leaving shareholders and bondholders standing. It is a courtesy that UBS has been careful not to reciprocate today. UBS’s current top management, not Swiss unlike those at CS, will happily retire in a few years. Here’s to Switzerland and the Swiss finding their own path to erasing this ignominious page in their history and limiting the long-term damage from the hasty decisions made a week ago.

In the meantime, we advise everyone who has lost money with CS to stick to UBS, a stock that can easily double thanks to the gifts of Swiss politicians. UBS is a company that was given CHF 54 billion in tangible capital, almost equal to the tangible capital it had before the takeover. Along with the capital they were given a strong profit-generating businesses and a huge franchise. The wealth management divisions of UBS and CS are strongly synergistic. CS’s Swiss commercial banking division is a jewel that, sold or combined with UBS’s division, can lead to huge gains or synergies.

A well-known investment bank calculates the value of synergies between the two realities at CHF 60 billion (CHF 8 billion annually capitalized). So, we are talking, in a far-from-blue-sky scenario, a gift of about CHF 114 billion, CHF 54 billion from the tangible equity given away and CHF 60 billion of the capitalized value of synergies. This is almost twice the current value of the company. To add insult to injury, the company is covered by the state for CS book losses in excess of five billion CHF and has a liquidity line of 100 BILLION CHF guaranteed by the central bank. Besides, it’s remained the only big Swiss (Swiss?) bank and must be defended to the death. It cannot be torn down.

In conclusion, if you lost money on CS, stocks, or bonds, hold your nose, and go where CS and your money are now, which is on UBS equity. To get it back!

Credit Suisse is dead.

Long live Credit Suisse!!

“There is no more champagne for everyone…”

I went to the wine shop a couple of days ago to buy a bottle of red. I noticed that on the champagne shelf, instead of the usual 75 cl bottles of Roederer there were awkwardly stacked 33cc boxes of the same product. I have always found a 33cc bottle of champagne a difficult creature to read, particularly when boxed. I took the liberty of asking the manager for enlightenment about the change in strategy. He looked at me and sighed. An expression of sadness and resignation overshadowed his face. Then, he lowered his gaze and explains. They are not delivering orders to him. It seems, he continued, that “THERE IS NO MORE CHAMPAGNE FOR EVERYONE…”

Mali famine 2022. Queueing up for food

In a world still full of adults and children who cannot access adequate nutrition, the phrase sounds like blasphemy or perfect for a line in a comic show. However, the reality is this, there is not enough champagne compared to the demand. Champagne supply is about 330 million bottles a year, demand is now slightly higher. The last time this happened, in 2006, champagne stock prices multiplied by a factor of three. In fact, if demand is higher than supply, the producers? tend to direct stocks to areas where prices are higher and then, gradually increase prices in the other areas. Considering the operating and financial leverage of these stocks, a 10 percent increase in the average selling price can more than double profits. However, so far, the sector has moved little. This is perhaps out of fear that what happened in 2007 will happen again: in the face of increased demand, the champagne appellation area was expanded, thus increasing supply. The great financial crisis and subsequent recession did the rest, causing the sector to lose between 60 and 80 percent. Moreover, today we start from the bottom, in fact these stocks trade well below tangible assets, a level never seen before, despite the catalysts we now see. It represents a fascinating risk/benefit profile…

[1] Six numbers that show why Credit Suisse has little leeway | Financial Times (ft.com)

Read More

“The good, the bad and the ugly”, Sergio Leone, 1966

Stagflation (THE UGLY)

As we anticipated, recession in the US is already a reality. Consumption data released a few days ago confirm this. US consumer spending fell month-on-month by 0.4% in real terms in May, while April’s figure was revised from +0.7% to +0.3%. A slightly negative June figure is likely. US consumer confidence is at a 16-month low. And that is not a negative. We continue to believe the current recession is only a technical recession, created by the collapse of the housing market, the securities market (stocks and bonds), cryptocurrencies, excess inventories accumulated during supply chain problems, and printing money. Between stocks and crypto in the US alone, the value of investments has fallen by USD 11 trillion, a huge amount (about 10% of Americans’ savings). It is a necessary recession to prevent inflation from becoming structural in the system. But it is transitory and probably limited to two/three quarters. Our view is absolutely very positive and absolutely not shared by the market.

Although every cycle is different, what happens to the stock market when rates are raised? It usually goes up. This is because the underlying economy is clearly strong, which is why rates are raised. A significant rise in rates, however, later leads to an economic slowdown, which, depending on the fundamentals, can lead to a hard or soft landing, i.e. a sharp recession or just a dampening of excesses. And that is why economists predict a recession in 2023, at the end of a series of upturns that would historically lead to a major slowdown. Why, instead, has the market been going down since the Fed’s first hike in March? The market is going down both because there was a massive tech bubble and then because of fears related to the repercussions of the return of the great monetary expansion that lasted a decade.

We believe that after the current technical recession linked to the rise in rates and the market crash, a recession in 2023 is unlikely to happen.  Why? 1) The housing market, residential and commercial, is not in a bubble. The imbalance between supply and demand is substantial as a result of years of under-investment linked to the scarcity of bank financing in this sector. The end of the pandemic will lead to a recovery in demand for office space and confirm the home as the place to work. Inflation is also another support for this asset class. 2) Consumption accounts for about ¾ of GDP in the US. Today’s consumption dynamics are negative, as is natural after the market crash and recession fears. However, the labour market is extremely strong and this is the backbone of consumption. The relocation of many manufacturing industries will maintain full employment and, along with this, a positive wage dynamic in real terms. Bonds finally provide attractive yields for savers. The stock market has corrected from the tech bubble and the traditional side is extremely attractive and will gradually appreciate again in the not too distant future. This tells us that consumption will be robust in 2023, recovering from 2022. 3) Corporate profits will nominally benefit from inflation, absorbing any inevitable pressures during a rate adjustment phase. In addition, many industries, such as finance, armaments, fossil fuels, and everything related to infrastructure and energy transition, will grow in the next 12 to 24 months. 4) There has been a shift in the US from an attitude of complacency towards inflation to one of strong fear. So much so that by now there is no longer talk of recession but of stagflation, something not seen for 40 years, in completely different environments (Volcker at the FED and Ronald Reagan in the White House). Today, however, inflation is coming down and gradually in the coming weeks and months we will begin to see it in the numbers. The fall in commodities prices these days and the gradual unwinding of the supply chain will contribute to this. The overstocking created precisely to address these problems in the supply chain will lead to substantial discount campaigns. The rate hike cycle will be powerful but entirely manageable, and we believe that the Fed’s current expectations of 3.8% for 2023 will not be revised upwards but may even be tweaked slightly downwards in the not-too-distant future (3.4% at the end of 2022).

Why? 1) The housing market, residential and commercial, is not in a bubble. The imbalance between supply and demand is substantial as a result of years of under-investment linked to the scarcity of bank financing in this sector. The end of the pandemic will lead to a recovery in demand for office space and confirm the home as the place to work. Inflation is also another support for this asset class. 2) Consumption accounts for about ¾ of GDP in the US. Today’s consumption dynamics are negative, as is natural after the market crash and recession fears. However, the labour market is extremely strong and this is the backbone of consumption. The relocation of many manufacturing industries will maintain full employment and, along with this, a positive wage dynamic in real terms. Bonds finally provide attractive yields for savers. The stock market has corrected from the tech bubble and the traditional side is extremely attractive and will gradually appreciate again in the not too distant future. This tells us that consumption will be robust in 2023, recovering from 2022. 3) Corporate profits will nominally benefit from inflation, absorbing any inevitable pressures during a rate adjustment phase. In addition, many industries, such as finance, armaments, fossil fuels, and everything related to infrastructure and energy transition, will grow in the next 12 to 24 months. 4) There has been a shift in the US from an attitude of complacency towards inflation to one of strong fear. So much so that by now there is no longer talk of recession but of stagflation, something not seen for 40 years, in completely different environments (Volcker at the FED and Ronald Reagan in the White House). Today, however, inflation is coming down and gradually in the coming weeks and months we will begin to see it in the numbers. The fall in commodities prices these days and the gradual unwinding of the supply chain will contribute to this. The overstocking created precisely to address these problems in the supply chain will lead to substantial discount campaigns. The rate hike cycle will be powerful but entirely manageable, and we believe that the Fed’s current expectations of 3.8% for 2023 will not be revised upwards but may even be tweaked slightly downwards in the not-too-distant future (3.4% at the end of 2022).

Jamie Dimon, CEO of the world’s largest bank and a keen observer who rarely says a word out of place, said a few weeks ago that he sees a storm coming. He doesn’t know if it will be big or small and the repercussions it will have, but he sees it coming. Where does this prophecy come from? Much of it has to do with the speed with which the Fed has decided to raise rates (from the current 1.75 per cent to 3.4 per cent at the end of 2022 and 3.8 per cent at the end of 2023) and the QT (quantitative tightening, i.e. the failure to reinvest the 9 trillion bonds held by the Fed as they mature) that has just begun in the US. This inevitably takes a lot of liquidity off the table in a short time. So some of the money earmarked for real estate or equity investments will inevitably end up buying bonds at (apparently) attractive yields, breaking the legs of speculation and in the short term depressing the real estate and equity markets. Moreover, the market anticipates the enormous volatility that these events can create. Indeed, the consequences of these manoeuvres are always difficult to define, particularly after the events of 2019, the last time the FED initiated a QT. At that time, bank reserves collapsed and REPO rates skyrocketed. So we think it is normal that there is some apprehension on the part of the banking system. However, today the banking system is better prepared (and Dimon himself states in the same interview that the banks are solid and ready) and the Fed has better control of the situation with adequate set ups to avoid a repeat of past tensions.

Elon Musk says he is super negative on the economy and will reduce the workforce by 10k. What entrepreneur isn’t, after the recent market crash and rate hike? Indeed, the US is in recession. However, let’s remember that Tesla has been hiring like crazy and it is right to take advantage of fears about the economy to lay off less useful workers in less efficient locations. Let’s remember that 10k laid-off workers is equivalent to less than a third of Tesla’s net hiring in 2021.

Meanwhile Warren Buffet has since the beginning of the year bought some USD 60 bln in stocks, including Paramount, Citigroup and Chevron.

In an article in the NYT over the weekend Paul Krugman (Wonking out: taking the flation out of stagflation) anticipates that, following the latest economic data, the Fed may soon revise the rate hike rate downwards.

The Economist seeks to respond to the hysteria of those who see a ‘Volcker moment’ today, i.e. the need to raise rates enormously to prevent inflation from entering people’s minds. The British weekly rightly points out that by the time Volcker intervened harshly on rates, throwing the country into recession, inflation had been rampant in the US for ten years. Today we are a long way from considering inflation or super inflation a companion.

Finally, Lawrence Summer, in an interview over the weekend, revises downwards his expectations on inflation (he was one of the first in 2021 to anticipate an inflationary wave and to oppose the Biden tax plan) and on raising rates, in light of the slowdown of the US economy in the first two quarters of the year.

To be balanced, we also report two interesting, slightly less recent and very negative podcasts by Greg Jensen, Co-CIO of Bridgewater. He expects prolonged stagflation in the US and believes inflation will remain out of control here for a long time. However, the thesis is not properly substantiated in our view. He advises investing in cheap assets that produce cash flow (with which we can only agree) and can benefit from inflation while advising to stay away from technology (still agree). He also advises diversifying away from the US, which they believe is priced for perfection, and investing in the rest of the world (also agree). He’s also negative on Europe where he sees an even heavier recession than he sees in the US (which as mentioned we don’t see but, even if we did, it’s already priced in anyway). Here Bridgewater has shorted 27 stocks in the Eurostoxx50 for around USD 15 bln (including many cheap stocks that produce a lot of cash flow). On the other hand, they have been very positive on China for some time and continue to be so even after the big losses and recent geopolitical events. On the dollar, they are negative and anticipate a long bear market as soon as the Fed approaches the end of its bullish cycle. They remain extremely negative on corporate bonds. In general, our opinion is that they see a delicate phase in the markets, with volatility and radical changes and they are betting on a few crashes, ready as always to cover quickly if they are wrong. In short, they are trying, but let’s remember that they are not the only ones and there is a lot of shorting in the markets today that will have to be covered sooner or later. Here are the links: Bridgewater Co-CIO Jensen on Investing Outlook – YouTube Bridgewater Co-CIO Jensen on Markets, BOJ Policy, Dollar – YouTube.

In Europe, many of the themes presented for the US market apply. With a few distinctions: 1) The European economy does not benefit but is hurt by the current price of hydrocarbons. 2) The risk premium associated with the Ukrainian conflict is significantly higher in Europe than in the US (and, at the same time, the end of the conflict will benefit stocks in this region much more significantly). 3) Inflationary pressures are lower in Europe as fiscal stimulus has been spread out more thinly than in the US. Future fiscal stimulus will continue to support the economy and the labour market in the second half of 2022 and in 2023. 4) In Europe there is less dependence of consumption on financial markets, which we believe will avoid a technical recession in 2022.

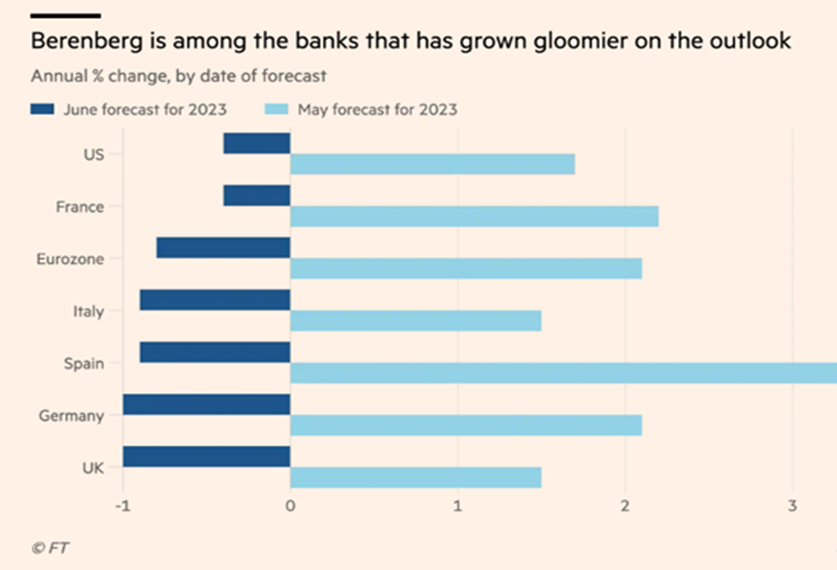

As in the US, we do not expect a recession in Europe in 2023 even in the event of a Russian gas cut. Talking to large German industrial companies, we do not perceive any particular fears. Clearly, forecasts are made to be proven wrong, and clearly the development of the war in Ukraine is decisive for the region. However, it is important to understand that the market now expects a recession in both Europe and the US in 2023. The large infrastructure investments, the post-covid reopening, the savings accumulated during the pandemic and a strong labour market are incompatible with a recession in our view, unless other new events occur. However, even if there were, it would have to be mild and is now more than priced in by the market, with cyclicals in many cases travelling at the levels of the March 2020 hole. We reiterate that now is the time to buy the much-hyped (and often overpriced) cyclicals in 2021 in view of the infrastructure revolution ahead and they are now trading at extremely low levels. Anticipation and diversification is essential. Below are Berenberg’s GDP growth forecasts for 2023 in May and June, which make it clear how the US rate hike and market downturn have distorted analysts’ perceptions. However, we believe the new forecasts are just as unreliable as the previous ones.

Financial Repression (THE GOOD)

We are living through a historic economic phase. Areas that, for various reasons, have suffered economic stagnation and deflation, such as Europe and Japan, are now about to embark on a journey that should return them to growth. It is an experiment, but there is so much at stake that all actors will make sure it succeeds.

From the post-war period until the late 1970s, much of the Western world reduced its war debt through so-called financial repression, i.e. through a level of interest rates slightly below inflation, achieved by banks buying up the debt themselves. Reducing debt in this way is politically more acceptable than raising taxes or reducing public services. The real rate of US short-term government bonds was negative from 1945 to 1980. Anyone who invested in British bonds between 1945 and 1960 would have lost over 1/3 of their purchasing power.

Actually, financial repression has been present in many areas since the great financial crisis of 2008, but as inflation was close to zero, the effects on debt reduction were insignificant. Now inflation has returned and, thanks to structural trends such as deglobalisation and the energy transition, it will not return completely. Through a constant inflation level, financial repression will bring its results. And it is the answer, the only possible answer for Japan and Europe. In a climate of financial repression, the creditor loses in real terms but the system in which it operates grows and develops, balancing these losses through gains on equity and real estate. In this context it will be appropriate to stay away from government bonds and invest in equities and real estate, and not only in inner-city residential but also in commercial and suburban areas, areas that lack of growth has often reduced to semi-abandoned dormitories. Restoring economic growth implies stimulating the demographic trend by accelerating the immigration process necessary to expand consumption and production.

In an editorial over the weekend Seth Carpenter, global chief economist at Morgan Stanley, says that given the rate forecasts released by the Fed Market Committee there is a willingness to accept higher-than-expected inflation for an extended period of time. The ECB seems even more in that camp. Japan is beyond that, continuing to monetise government debt and keeping rates at zero. When inflation finally kicks in vigorously in Japan as well, we would not be surprised if the debt held by the BOJ (about 35%) is wiped out, setting the stage for the last mighty leg of yen devaluation and the recovery of the Japanese economy.

Here is a link to an interesting podcast by Professor Russell Napier, where he talks about financial repression: Professor Russell Napier: The equity index fund is a dangerous product – YouTube

War (THE BAD)

Russia has captured the last city of Luhansk, one of the two regions that make up the Donbass, the area of the country that Putin promised to ‘liberate’. This represents a major victory for Putin, who needs to demonstrate his successes in order to balance heavy losses and growing internal discontent. At the same time, the new HIMARS mobile launching stations provided by the US to Ukraine are beginning to take effect, destroying Russian weapons depots and command centres with great precision. More will come in the coming weeks. Apparently, the war cannot end until the whole Donbass is in Russian hands. However, several commentators seem to indicate that Russia, after the last dramatic blow to conquer Luhansk, which brought huge losses to the army, is now finding it difficult to proceed further and, at the same time, keep control of the already conquered territories. Russian missiles fired haphazardly at the rest of Ukraine may indicate this. Anything can still happen. Russia may now have an interest in sitting down to negotiate, keeping part of the Donbass and releasing other territories. Ukraine will surely want to continue the war to retake occupied territories and demand damages. The Western world intends to penalise Russia and the Putin regime but, at the same time and without clearly admitting it, to avoid the risks of Russia using tactical nuclear weapons. So it will provide the necessary weapons to balance the forces on the field, nothing more. Today the consensus is for a very long war. And we believe this is indeed a possibility, already well digested by the market. However, we do not exclude that in the course of the next few weeks things may change. Ukraine’s fear of the launch of tactical nukes on Kiev may soften their stance. Indeed, Russia could use the recent Ukrainian missile attacks on depots on Russian territory to threaten missile repercussions on the capital and possibly the very use of tactical nukes. Against this the West has no weapons, not wanting under any circumstances to risk a nuclear war. As always, in the absence of a clear winner, both sides have a lot to lose in order to reach the negotiating table. We believe we are not far from that point.

Any news of opening negotiations would have a significant positive impact on world markets, especially European markets. It would also lead to lower gas and oil prices, easing inflationary fears.

Read More