Apple crumble(s)?

The long-awaited ruling in the case brought by Fornite against Apple’s misuse of its Apple Store platform came out this week. From now on, Apple will have to allow iPhone owners to purchase apps outside of the Apple Store, i.e. without paying Apple the 30% “fee” for using “its” software.  Every app found in the Apple Store will now have to display a link to its original website where the app is free. This is a good victory. The judge hints that it could have gone further, allowing people to bypass the Apple Store and download apps by placing the icons of externally purchased apps directly onto the home screen of the iPhone. However, Fornite’s lawyers were unable to prove Apple’s position of monopoly. Fornite will not return to being available to Apple users until it has achieved a full victory, which we believe will inevitably come sooner or later. When this time comes, the owner of an iPhone will be able, as he should be, to freely dispose of his phone. Apple will be free to offer services on its platform, but in competition with other providers. We believe that Apple’s big growth in services, the driver of the stock, will not materialise as strongly as hoped. It should be noted that the US Department of Justice considers the contribution of 10 billion USD a year that Google pays to Apple to use its browser illegal. Once again here, Apple is unlikely to prevail. It is true that 10 billion USD is just 4% of Google’s revenues, but since there are practically no costs linked to this service, this amount should be compared to gross profit, of which it represents 12%. The optimists will say that these items should not be considered so much in the face of Apple’s secular growth and exceptional positioning. We are not so sure.

Every app found in the Apple Store will now have to display a link to its original website where the app is free. This is a good victory. The judge hints that it could have gone further, allowing people to bypass the Apple Store and download apps by placing the icons of externally purchased apps directly onto the home screen of the iPhone. However, Fornite’s lawyers were unable to prove Apple’s position of monopoly. Fornite will not return to being available to Apple users until it has achieved a full victory, which we believe will inevitably come sooner or later. When this time comes, the owner of an iPhone will be able, as he should be, to freely dispose of his phone. Apple will be free to offer services on its platform, but in competition with other providers. We believe that Apple’s big growth in services, the driver of the stock, will not materialise as strongly as hoped. It should be noted that the US Department of Justice considers the contribution of 10 billion USD a year that Google pays to Apple to use its browser illegal. Once again here, Apple is unlikely to prevail. It is true that 10 billion USD is just 4% of Google’s revenues, but since there are practically no costs linked to this service, this amount should be compared to gross profit, of which it represents 12%. The optimists will say that these items should not be considered so much in the face of Apple’s secular growth and exceptional positioning. We are not so sure.

Some people think that our judgement of Apple is based on an aversion to the company and the product. This is absolutely not the case as we all have apple products, from desktops to laptops, watches, iPods, and iPhones – this is the point we are trying to make. Where else can the company grow if not in services? And how will it grow if its services are no longer privileged? Growth in emerging countries is saturated and growth linked to expanding the offer with cheaper models has already been pursued. So? Apple has not been able to create anything original since Jobs’ decease, so why should it now? It could have embarked on the electric car with Musk, but instead it snubbed him. It could have created virtual reality devices, but it left that to FB and Sony. It could have become a leader in electronic payments, but here too, it was unable to capitalise on its position. Why should it now become a leader in these areas? It should also be noted that news came out this weekend that Doug Field, former Tesla manager and head of Apple’s Titan project which aims to produce electric cars, has left Apple for Ford.

Apple has eaten all the cash in its belly, shooting it to shareholders through aggressive buy backs. It is true that it produces 70 billion in cash each year, but if it stops returning this money, we doubt that the stock will respond well. Also in order to invest, you need idea’s.

The hardware it produces is not innovative and the brand is starting to get boring and worn out. It’s true that it is a luxury and status symbol, but luxury in consumer electronics has never lasted, at least so far. We wonder if a fresh new product could put Apple into times of difficulty. Slinking away as if the Behemoth has given up on the fight. Anything can still happen, and it’s stock has never been so strong. Moreover, such a large company has immense media power. Despite this, we can’t stop the smell of apple crumble from wafting up our noses.

Atos, a disaster. Good!

We met with Atos last week following the announcement that they plan to carve out and divest its legacy businesses (those that are downsizing due to the migration of information systems to the cloud.) By trying to read into the body language of the CEO and CFO it seemed to be the case that: 1) the carve out is technically difficult; 2) finding a buyer for a forced sale is even more difficult; 3) the demand for the business is still very good, 4) they have problems with HR retention being stolen by competitors; 5) the CEO has 80% of his family wealth in the company’s securities (the rest is the house!). We infer that something will have to happen soon. Though the management are burnt out, at the same time they know the company inside out and are positive about the firms outlook. If we add to this fact that Goldman Sachs, as precise as a moving average, downgraded the company a few days ago and that the stock has been kicked out of the CAC, we cannot help but continue to be positive about the company.

Atos Vs Capgemini a 10 anni

Fonte: Thomson Reuters

Korean dawn

Korea, a nation that has always been somewhat neglected, is surprisingly emerging.

La band BTS

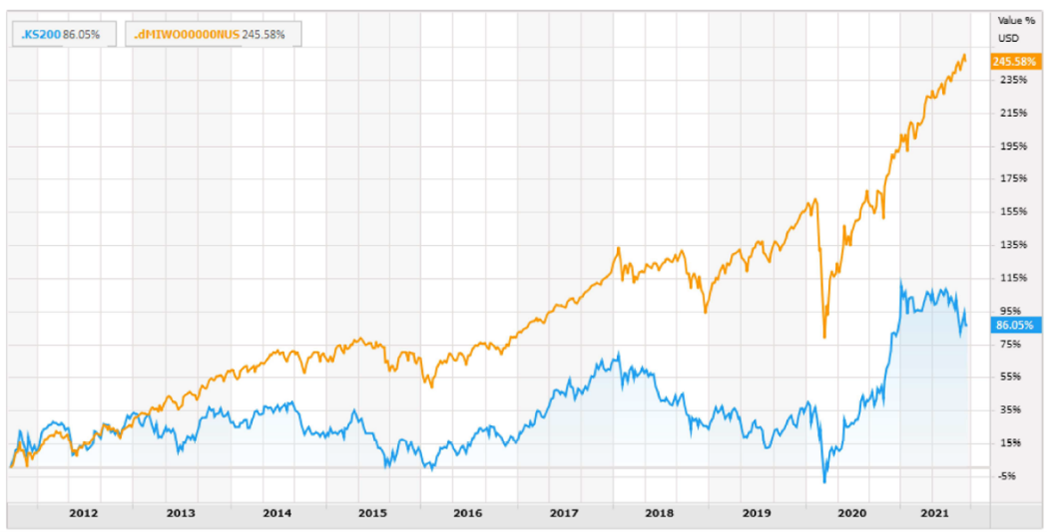

In film, music, fashion and food and wine.  Their electronic products, once seen as a proxy for Chinese ones, are now increasingly refined and luxurious. Their automotive brands are growing significantly. And the market, after years of slumber, has woken up and in the last year and has at least stopped underperforming in the MSCI World (chart). South Korea invests more in R&D than any other country in the world. It has very high productivity and low public debt, solid democracy, reliable budgets, strong banking systems, an excellent central bank, and corporate governance is improving incredibly fast. And valuations are among the lowest in the world. If all this sounds delicious, add to it a free option on the reunification of the two Koreas.

Their electronic products, once seen as a proxy for Chinese ones, are now increasingly refined and luxurious. Their automotive brands are growing significantly. And the market, after years of slumber, has woken up and in the last year and has at least stopped underperforming in the MSCI World (chart). South Korea invests more in R&D than any other country in the world. It has very high productivity and low public debt, solid democracy, reliable budgets, strong banking systems, an excellent central bank, and corporate governance is improving incredibly fast. And valuations are among the lowest in the world. If all this sounds delicious, add to it a free option on the reunification of the two Koreas.

Modelli di del famoso stilista coreano Hyein Seo

Kospi 200 Vs MSCI World Net 1 anno

Kospi 200 Vs MSCI World Net a 10 anni

Fonte: Thomson Reuters – USD

The Thaw

Who said physical banks are no longer needed? SBI Holding, Japan’s online financial boutique launches a bid on 48% of Shinsei bank, a smaller government-controlled bank, with the aim of restructuring the bank and offering a service platform for regional banks. Shinsei after rallying 30 percent to reach the offered price is still only worth 0.4x the tangible equity and less than 9x of the earnings. SBH wishes to restructure Shinsei into a service platform for regional banks. SHB is held mostly by Western investors. M&A is gradually emerging in Japan and is only at the beginning of a process that will gain momentum.

Dialogue between a value investor and a growth investor

The growth investor asks himself “Why be a value investor?” Why go after dead or otherwise struggling companies rather than celebrate the inevitable success of the winning ones? Why spend your time hoping that the sick one will recover rather than following the virtuous athlete? Why expose yourself to unpopular topics where, if you make a mistake, the clients and observers will mortify you and question your professionalism, rather than exposing yourself to popular topics where no one is ever responsible?

“The answer is simple”, retorts the value investor. Here, if you are disciplined and not too emotional (greedy or timid), the chance of making money in the long run is greater. Betting against the herd in the long run pays off and today, the elastic of the valuation gap is so tight that it is friendly. But there is another reason. One that is absolutely counterintuitive but true and is linked to the very pleasure of investing in value. Value is life and joy. Growth is death and disappointment.

The value investor addresses Kahlil Gibran,

“I feel like a field sown in the heart of winter, and I know that spring is coming. My streams will begin to flow and the little life that sleeps in me will rise to the surface at the first call”.

Following a lifeform in its difficult recovery, waiting for spring, is a hymn to life. On the other hand, every beauty finds old age, every famous politician finds his defeat, every great love has its disappointment, and every Sunday and every summer brings with it Monday and autumn. Value is future and joy. Growth is past, sunset and disappointment.

The growth manager shakes his head unconvinced, reflects, and then quotes a verse from Antoine de Saint-Exupéry’s The Little Prince,

“Of course I will hurt you. Of course you will hurt me. Of course we will hurt each other. But this is the very condition of existence. Becoming spring means accepting the risk of winter. To become Presence is to accept the risk of Absence”.

The growth investor explains that one must accept the inevitable transience of the most beautiful and virtuous things (societies) rather than fear it. You have to live with it, enjoy it and then, when the time comes, let it go.

The growth investor then cites a recent article by Gil Parkinson of Aviva (click here to view it) who points out that the intrinsic value of a company can be far from what is expressed by financial statements, and that investors who fixate on low multiples will ultimately be disappointed.  To support this theory Parkinson talks about Graham, pointing out that almost half of Graham’s returns from 1948 to 1972 came not from his net worth, but from his investment in Geico; thus, a single small company grew immensely both in size and value, multiplying over 500 times in 24 years.

To support this theory Parkinson talks about Graham, pointing out that almost half of Graham’s returns from 1948 to 1972 came not from his net worth, but from his investment in Geico; thus, a single small company grew immensely both in size and value, multiplying over 500 times in 24 years.

The value investor listens attentively and then calmly retorts. He does not deny that many companies with high multiples have or will have enormous potential and can multiply in value many times over, but that such potential is not so easily identified. It is like judging the desirability of becoming a footballer by looking at Ronaldo’s salary, forgetting all the promising footballers who have invested so much and then failed. The level of understanding of the individual business and its competitive, regulatory, technological evolution and associated risks must be extreme and often not enough. If you get it wrong, the wake-up call can be shocking as you fall way off the mark. By focusing on the numbers on the balance sheet and modest valuations, which is what the value investor does, the upside may be smaller, but the investment case is more straightforward and dependent on factors on which well-defined assumptions can be made. Finally, he also points out that in 1972 GEICO was worth $72, while in 1976 the same company’s stock price had gone down to only $2.

In the end, growth and value investors agree that each has their own reasons. And they both should be respected. The important thing is that there is a method, discipline, consistency, transparency and professionalism, whatever the method applied.

Back