These days the old adage attributed to Nathan Rothschild, “Buy on the sound of cannons, sell on the sound of trumpets,” comes to mind.

A recession 2/3 years after the pandemic, until a few months ago an entirely remote possibility. Such a possibility was not completely discarded by the market just out of superstition. Like when you fear missing your plane to go to the all-inclusive resort in the Maldives, after dreaming about it for years, even though you know in your heart that you will not miss it.

In just a few weeks, recession has become a certainty.

Trying now to rise above the background noise, let us take a look at the cyclical stocks, those that will have to suffer most, alas, from the recession.

Today residential builders in the U.S. are near -50% from their highs of the past twelve months (D. R. Horton and Lennar -45%, KB Home -51%, Redfin -80%). Banks range from-35%(JPM, Bank of America, Wells Fargo) to over -40% (Citigroup). Insurance companies from -20% to -40% (Metlife -17%, Prudential -25%, Lincoln -39%). Transportation companies, those most anticipating a recession, from -30% to -40% (Fedex -29%, UPS -27%, DPW -43%), retailers from -30% to -50% (Home Depot -35%, Kohls -38%, Macy’s -47%, Target -48%), cement and building materials from -30% to -60% (Martin Marietta -31%, Vulcan Materials -31%, CRH -34%, Tutor Perini -58%), finally, automotive by more than 50% (GM -53%, Ford -56%). All the sectors mentioned are not comparable with the same sectors in 2007 or even 2020. Today they are much stronger and have better medium-term prospects. In addition, the consumer is less indebted and scared.

Banks range from-35%(JPM, Bank of America, Wells Fargo) to over -40% (Citigroup). Insurance companies from -20% to -40% (Metlife -17%, Prudential -25%, Lincoln -39%). Transportation companies, those most anticipating a recession, from -30% to -40% (Fedex -29%, UPS -27%, DPW -43%), retailers from -30% to -50% (Home Depot -35%, Kohls -38%, Macy’s -47%, Target -48%), cement and building materials from -30% to -60% (Martin Marietta -31%, Vulcan Materials -31%, CRH -34%, Tutor Perini -58%), finally, automotive by more than 50% (GM -53%, Ford -56%). All the sectors mentioned are not comparable with the same sectors in 2007 or even 2020. Today they are much stronger and have better medium-term prospects. In addition, the consumer is less indebted and scared.

In Europe, courtesy of war, we find the same retracements in the cyclical sector, albeit with even lower valuations.

Is recession inevitable? We believe not, and we continue to think, contrary to what the market thinks, that we will see a technical recession in the U.S. this year and no recession next year. But prognostications, as we know, leave time for themselves and what matters is still the risk/return profile. So is recession discounted in cyclical prices? We think so. Instead, we would stay away (for much longer) from bubble-object tech and so-called “quality” stocks whose quality, with slowing and rising rates, will soon be tested. And since they are on valuations between 50 and 100 percent above market valuation, it will be appropriate for them to confirm it. Finally, watch out for pharmaceuticals as well. Although optically not expensive on earnings, they nonetheless have very juicy margins (they all now stand between 3x and 5x sales), just as the Biden administration is trying to reduce the cost of prescription drugs in the U.S., the geographic area from which almost 2/3 of the industry’s profits come on average.

We waste time trolling the companies we are invested in. We read what they publish. We pester them with bold inquiries about how they compile their sustainability reports (they often don’t know) or to understand the numbers on their balance sheets or to investigate how things are going in general. What we observe is that those that do not sell commodities (metals, paper, fuels, etc.) tend to update prices with some delay because old contracts do not consider surges such as we have seen recently. Wages also require some negotiation before they are raised. What we mean is that inflation is like a boat, you know it’s going to turn if you move the tiller, but it has that thing, which in sailing terms is called a draft, that creates a time lag. We believe that galloping inflation, the terror of every central banker, is now under control. The market crash and rate movement have restored order. But it takes time before it shows up in the numbers. The risk is clearly that a restless and pressured central banker will kill the patient with too heavy and unnecessary therapy. These things the central bank knows, and it also knows that it has to show itself to be bad in order to kill what are called the “animal spirits” of the market, that is, the human positivity reflected in the rise of the markets, a rise that is itself inflationary.

Much of the decline has already taken place, just as much of the inflation has already run its course. Excluding technology, which lives a life of its own, anticipating very future growth, and the CD quality stocks, which we have already discussed, the U.S. market is attractive again today. The European one is worth a song and remains tied to energy normalization and the end of the war. The Japanese one is always exceptionally cheap, with a central bank that, no doubt in agreement with the U.S., is powerfully reflating the patient and bringing it back to life after thirty years of deep coma. On the other hand, the U.S. today needs a strong Japan that can guard a sensitive area well. Korea seems to be following the U.S. market and presenting the same buying opportunity it presented in March 2020. Meanwhile, many of the emerging markets are benefiting from the commodities super cycle.

Robert Armstrong, a nice and good journalist at the FT, talks this week about the downward revision of corporate earnings (click here to read the article). After premising that at 15.2x 2023 earnings the S&P cannot be considered expensive, the journalist nevertheless speculates that if instead of a 10 percent rise in 2023, as expected, we were to find ourselves with a 10 percent decline, the S&P would go from 15.2x to 18.5x earnings. In an area certainly not cheap. Well, assuming a 10% rise in earnings for 2023 actually amounts to predicting flat earnings, because of inflation for the period. So a 10 percent decline in S&P earnings in 2023 would be equivalent to a 20 percent decline in real terms and would be something dramatic, similar to what we saw in 2020 (Covid) and only less than what we saw in 2008, during the worst financial crisis since ’29. These P/Es are then still the consequence of the strong presence of tech and “quality” stocks inside the S&P. In our portfolios it is difficult to find stocks above 10x earnings and about half trade below tangible equity. Let’s be clear that we are not talking about a few extreme situations; in fact, we have in the various products about 500 stocks. As mentioned above, the situation is reminiscent of the 1970s, when stocks in the real economy were extremely depressed.

We are all scared of R, but there is never a better opportunity than a recession to make significant gains, with the exception of those accompanied by a financial crisis. The latter are long and very dangerous. Best to stay away from them. Today, however, the financial system is sound, as confirmed by James Dimon himself, respected and influential CEO of JPM, and will hold up well to the shock wave.

An average bear market lasts about nine months with declines around 36 percent. Under this assumption, we would touch lows in October with a further 17 percent decline from current levels in the S&P500 index. Certainly not a modest amount of downward space. But let us remember that we are talking about statistics that incorporate bear markets such as the very long one of 2000-2003, the one of the great financial crisis and the huge crash of March 2020. Moreover, from the beginning of the bear market to the end, an inflationary wave, as mentioned, will have protected the downside of the index, which, as we know, expresses nominal and not real magnitudes. In the last twelve months the U.S. CPI has risen 10 percent and in the next twelve months it is reasonable for it to rise 6 percent. So in real terms we are already close to the 36% mentioned. Moreover, in view of the financially sound system and good prospects on the investment front (infrastructure, energy transition, deglobalization) it is plausible that, even in the event of a recession, the downturn should be milder than the average of previous ones.

Therefore, the summer months present an opportunity to invest and position carefully, judiciously, and diversified. Before the market, like a jackrabbit, quickly changes direction, right at the peak of negativity, starting to paw, cheerfully and for no apparent reason, toward an uptrend. The next upswing will be based less on speculation and more on the real economy and will have real repercussions on the latter.

R for rabbit…

ATOS

In the last week, Atos, a stock in which we have significant positions, at least for us who consider diversification vital, lost 50 percent. After it had lost in the previous 12 months already 60%. One might think that this is a stock subject to the Nasdaq bubble. Nothing could be further from that. The stock is one of the titans of IT consulting, with over 110k professionals on the payroll and 11 billion euros in annual revenue. The stock before the collapse of the last 5 days was trading at about 0.4x EV/SALES versus a market trading between 2x (CapGemini or Reply) and 3x (Accenture). Here the problem was governance and management after the departure of Thierry Breton two years ago, who left to become EU Commissioner. A dirigiste chairman of the board, Bertrand Meunier, and a CEO probably without the necessary experience, Elie Girard, produced a series of major mistakes. Earlier in the year the hiring of Rodolphe Belmer, an experienced manager responsible for the successful turnaround of Canal Plus, as the new CEO gave hope to the market. These painfully cleaned up balance sheet (kitchen sinking) and brought the company back to growth in the first quarter. Since his arrival the company has also hired about 10k new professionals (net of departures). Certainly an encouraging sign.

Nothing could be further from that. The stock is one of the titans of IT consulting, with over 110k professionals on the payroll and 11 billion euros in annual revenue. The stock before the collapse of the last 5 days was trading at about 0.4x EV/SALES versus a market trading between 2x (CapGemini or Reply) and 3x (Accenture). Here the problem was governance and management after the departure of Thierry Breton two years ago, who left to become EU Commissioner. A dirigiste chairman of the board, Bertrand Meunier, and a CEO probably without the necessary experience, Elie Girard, produced a series of major mistakes. Earlier in the year the hiring of Rodolphe Belmer, an experienced manager responsible for the successful turnaround of Canal Plus, as the new CEO gave hope to the market. These painfully cleaned up balance sheet (kitchen sinking) and brought the company back to growth in the first quarter. Since his arrival the company has also hired about 10k new professionals (net of departures). Certainly an encouraging sign.

The surprise. A few days ago Belmer was fired, and the company unveiled a strategic plan (click here to access the presentation) that may make sense on paper but lacks the CEO’s support. The plan is based on splitting the infrastructure division from the digital and cybersecurity (BDS) divisions. Split to be done within two years. Belmer, on the other hand, wanted to sell the BDS division, which accounts for 12 percent of sales for which he had received an offer from Thales for 2.7 billion euros (the company before the collapse was worth 4.8 billion considering debt of 2 billion). Airbus also seemed interested in taking it over for more than 3 billion. Selling BDS would have left the restructuring infrastructure division to be managed in the future as a cash cow and the digital division whose growth could be revived.

Faced with management’s show of disagreement and the final decision to pursue a strategy that the recently hired CEO did not believe in, hedge funds jumped in to sell short. Other investors (including us) dismayed tried to make sense of it all. Meanwhile, to make the HFs’ job easier, the French government was issuing a statement specifying how the company could not be subject to takeover.

ATOS vs CAPGEMINI 3Y Total Return

Source: Thompson Reuters

Unfortunately, these things happen. The time to return on capital gets longer but potentially the return increases. Despite the understandable disappointment, there is no reason for the stock to trade at these prices, regardless of strategy. The right management will eventually be found. The company has unique divisions of the highest quality. We believe that the crisis in the infrastructure sector at 12 months will have receded due to the reduction in supply and the trend of industry consolidation. The support of the French state, the company’s first customer, is unconditional. Pessimism and shorting on the stock are extreme. There is no risk of false accounting or bankruptcy. The BDS division can at any time be liquidated at a valuation now equal to the value of the entire company, including debt.

We are therefore buying back the stock, always within the framework of proper diversification and risk control.

Read MoreIn these last few days, the desire to stay invested in equities is understandably being put to the test.

As we know, there are many problems, but let us try to put them in perspective together with the opportunities that tend to be forgotten at these junctures.

Rates go up. Rising rates take liquidity off the table and therefore less leverage and less investment. However, more ‘normal’ rates help the profitability of the financial system, reduce corporate and public pension deficits and increase savers’ returns. In addition, rate normalisation reduces speculation, the enemy of long-term real growth. As for mortgages and the real estate market, let us remember that a family buys a house when it is confident about the future of its job, and a 2 per cent higher interest payment is only decisive for the highly leveraged real estate company.

Inflation is very high, not far from 10%, in both the US and Europe. However, 1/3 of that in the US and 2/3 of that in Europe derive from the volatile components related to food and oil, now under pressure as a result of the war. Once the war is over, the rate should gradually fall to levels close to, but above, 2%. However, this inflation wave is important to stimulate the economy in areas like Japan and Europe, which have been locked in a deflationary grip for years. While it is true that inflation initially weighs on the consumer, it is also true that it then reactivates the wage dynamic, stimulates the real estate market, particularly in secondary areas, and makes listed companies linked to the real economy, with plants and assets, even more attractive, those that are now on the value side. While it is true that some sectors may initially suffer in terms of profits, it is also true that in the medium term almost all companies post higher profits in an inflationary environment, at least nominally. Finally, inflation reduces public and private debts.

High oil, gas and agricultural commodities represent a tax on the consumer. However, they also represent a huge incentive to invest heavily in energy and food, sectors that are crucial not only from an environmental and social point of view, but also because they are highly capital intensive. Agriculture means fertilisers, seed, farm machinery and land that gains value. Energy means renewables, grids, pipelines, hydrogen, as well as stimulating the growth of gas supply through more upstream investments. We are talking about hundreds of billions of dollars of increased investment over the next three to five years as a result of the anomalies that emerged with the war. This creates a powerful flywheel that feeds aggregate demand.

War is a dramatic event. Not a day goes by without our thoughts going to the families devastated by the conflict. However, wars end. And this one will be no exception. The longer the war lasts, the more volatile the markets will be, but the greater the likelihood that Putin’s regime will end. A long war will be difficult to explain even for a totalitarian regime. Once it is over there will be hundreds of billions of euros to spend on rebuilding Ukraine. Europe will finance a large part of the reconstruction and benefit proportionally.

So much we complain about supply chain bottlenecks, but little is said about the fact that these are an integral part of the deglobalisation process that will bring so many important manufacturing processes back in-house, supporting the already strong labour market.

The announced global fiscal stimulus has yet to be released to a large extent and will support the above trends, particularly in Europe, Japan and Korea.

The ECB has disappointed to some extent. True. Having already prepared an instrument against another eurozone crisis (‘fragmentation’) would have been wise. It probably takes some tension in the markets for it to be prepared, otherwise there is a lack of political support in the Netherlands or Germany. Today, however, another eurozone crisis is highly unlikely as it is known that in that case the ECB would certainly intervene clearly and quickly, with instruments that are already known and effective.

Even in the event of a technical recession, it is better not to bet on sharply downwardly revised profits. The dynamics described, in addition to the desire to restart after the pandemic, and the over-savings accumulated during it by households, will act as an impulse for consumption.

Against a backdrop of war, inflation, the end of QE, tech bubble deflation and with a likely tech recession in the US coming, it may seem easy to bet against the market and follow the trend these days. We wouldn’t. If these themes keep the market capped for now, the above arguments create important support for it. It will continue sideways and this will give the most flexible people a chance to buy on weakness (not tech) and release on strength. We should probably wait for the technical recession in the US with the inevitable inflationary slowdown to lift the stops and enjoy a significant market rerating, starting with Europe and Japan. Since the downside of the market today is limited (traditional/value side) we believe it is better to stay there and take advantage of these stressful phases to accumulate financially sound stocks with a good franchise and low or very low valuations. And you are spoilt for choice….

Panta rei

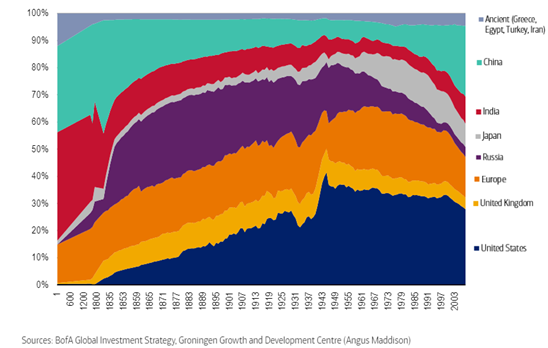

A couple of weeks ago Bank of America published a report by Peter Harnet in which a very interesting graph appeared. It illustrates the breakdown of global GDP by geographical area in different historical periods. So you can see that 2000 years ago China, India, Greece, Egypt and Turkey accounted for 84% of global GDP. In the mid-1800s Russia and China accounted for about 40%. Communism reduced them greatly. In particular, Russia went from 30% in 1800 to its current irrelevance, probably made even more extreme by the recent conflict. While China returned to growth with the advent of Deng Xiaoping’s ‘market socialism’, rising from 5% in the 1970s to 25% today. The growth following its inclusion in the WTO in 2001, which marked the beginning of the extreme phase of globalisation, was dramatic and coincided with the reduction in weight of Western countries. Japan grew from nothing to 5% with the economic expansion of the Meji era (1868-1912) that ended the shogunate and samurai rule. The Second World War heavily downsized Japan, which then, however, from 1960 to 1990, rode two phases of exceptional growth that brought it up to 14% of global GDP. Almost 30 years of deflation and bear market then brought it back to 6%, and now there are signs of stabilisation. Britain experienced its heyday in the Victorian period and has always declined from there, although less than Europe. The next few years will see the results of Brexit on the country. Europe managed to stay relevant for 2000 years, with relays between the Romans the French and the Germans. The peak was reached in the 1960s and 1970s with the creation of what would become the European Union. Unfortunately, there was then a gradual decline that accelerated dramatically with China’s entry into the WTO. After that phase, Europe lost about 10% of global GDP. India has also remained relevant over time. After the glories of 2,000 years ago, when its GDP was larger than China’s and touched almost 40% of the global GDP, there was a gradual decline in importance that became more pronounced with the departure of the British and the partition of the country. A country with great resources but a confusing democracy, India remained at around 5% of global GDP throughout the 20th century and is now showing signs of revival, unfortunately, as is often the case, with a democracy with autocratic overtones. Finally, the United States. They are those among the Western countries that have been best able to manage globalisation, limiting their loss of weight, which nevertheless amounts to 5% since 2001.

Everyone can draw their own conclusions. We limit ourselves to a few reflections.

An autocratic government that does the right things can often accelerate the country’s growth, but if it does not, it can easily be the cause of the country’s demise. So for investment, a democracy, however imperfect, is always preferable.

While recognising the merits of globalisation, it was badly set up and led to an adjustment too fast. The results are there for all to see, with a West dependent on a powerful, autocratic, belligerent China with completely different values from the West.

Russia seems ready to hit rock bottom and we would not be surprised if this mad war represented the final stage of its dramatic decline.

Europe could probably find in a true union the solution to get out of the decadence in which it finds itself. While it is still difficult to be optimistic on this front, we can say that we are more so than we were three years ago.

Global GDP breakdown by geographical region over the past 2000 years

Back Read More