Plaza Hotel

The famous New York hotel took several decades, from 1883 to 1907, to reach its current form. This period was characterised by several changes of ownership, bankruptcies and court actions. The architect responsible for the current style was Henry J. Hardenbergh, who, at the request of the then owners, was inspired by the architecture of the Loire chateaux.  Today it is divided into a residential part, consisting of exclusive accommodation, and a part managed by Fairmont as a luxury hotel. The hotel is a little old-fashioned for our tastes, but it does have a bar/restaurant, The Palm Court, which is a must for lunch, dinner, drinks or even just tea during a visit to the Big Apple. More than 40 internationally famous films have been set at the Plaza, including ‘North by Northwest‘ with Cary Grant (1959), ‘Cotton Club’ with Richard Geere (1984), ‘Scent of a Woman‘ with Al Pacino (1992) and ‘The Great Gatsby‘ with Leonardo DiCaprio (2013). However, it doesn’t end there. In September 1985, in the meeting room of the Plaza Hotel in New York, the G5 (USA, Japan, UK, France and Germany) signed the Plaza Accord, which defined a concerted action of the governments and central banks of these countries aimed at a pilot devaluation of the dollar.

Today it is divided into a residential part, consisting of exclusive accommodation, and a part managed by Fairmont as a luxury hotel. The hotel is a little old-fashioned for our tastes, but it does have a bar/restaurant, The Palm Court, which is a must for lunch, dinner, drinks or even just tea during a visit to the Big Apple. More than 40 internationally famous films have been set at the Plaza, including ‘North by Northwest‘ with Cary Grant (1959), ‘Cotton Club’ with Richard Geere (1984), ‘Scent of a Woman‘ with Al Pacino (1992) and ‘The Great Gatsby‘ with Leonardo DiCaprio (2013). However, it doesn’t end there. In September 1985, in the meeting room of the Plaza Hotel in New York, the G5 (USA, Japan, UK, France and Germany) signed the Plaza Accord, which defined a concerted action of the governments and central banks of these countries aimed at a pilot devaluation of the dollar.

During the week, there was an internal debate about what Japan would be like now if that agreement had never been concluded, and whether the country’s 30 years of suffering were essentially due to that event. To better understand this, we need to go back in time.

On the 15th August 1945, following the release of two atomic bombs on Hiroshima and Nagasaki, the Japanese surrendered unconditionally. The decision to drop the bomb on Hiroshima on the 6th August could have been avoided as Japan was already defeated. Furthermore, the decision to drop the bomb on Nagasaki three days later, on the 9th August, without even giving the Japanese time to realise what had happened in Hiroshima, was criminal. The American military leadership, including future US President General Dwight Eisenhower, was against the use of the bomb. General Curtis Le May, famous for his aggressiveness, stated in September 1945 that the two atomic bombs were not the reason the war was over. In another world Harry S. Truman, the man who gave the order to drop the first and then the second bomb, would not be so well remembered and celebrated. Yet, we know at the end of the day, winners write history.

Furthermore, the decision to drop the bomb on Nagasaki three days later, on the 9th August, without even giving the Japanese time to realise what had happened in Hiroshima, was criminal. The American military leadership, including future US President General Dwight Eisenhower, was against the use of the bomb. General Curtis Le May, famous for his aggressiveness, stated in September 1945 that the two atomic bombs were not the reason the war was over. In another world Harry S. Truman, the man who gave the order to drop the first and then the second bomb, would not be so well remembered and celebrated. Yet, we know at the end of the day, winners write history.

After the war, Japan spent a few difficult years under American rule. However, during that domination, Japan’s semi-feudal political-economic system was partly dismantled, and structural reforms were introduced. This, together with the plan for the country’s revival that the US helped to finance. As the Japanese cultural system is based on meticulous organisation and dedication to work, this gave rise to the Japanese economic miracle that saw the country rise powerfully from its ashes and outperform all Western countries from 1955 to 1985.

Although, in the mean time, The United States became the hegemonic power on the planet; it grew and expanded, cashing in on dividends from a great war it had won whilst also benefitting more than proportionately from the global recovery. However, towards the end of the 1960s a series of problems arrived that slowed growth: Vietnam, the oil crisis, and inflation. The US fought inflation at the cost of economic growth, but by 1983 inflation was defeated and the economy was recovering. It was the time of Reaganomics, based on supply-side theories, and the desire and need to take back lost opportunities. While fighting inflation, Volcker raised interest rates dramatically (80-82) and then when Reagan came in, the nation’s fiscal policy was rapidly expanded (’83-’84). This led to an increase in the value of the dollar and the US trade deficit. All the while, out there were countries like Japan and Germany, enthusiastic about producing and less so about consuming. Somehow the US needed to balance its deficit.

This all led to the Plaza Accord. The US used moral suasion to persuade the two great losers of the Second World War to accept a resetting of exchange rates. But while Germany was cautious, Japan appeared enthusiastic. This was a chance to play a decisive role in the world political arena again.

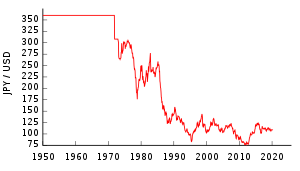

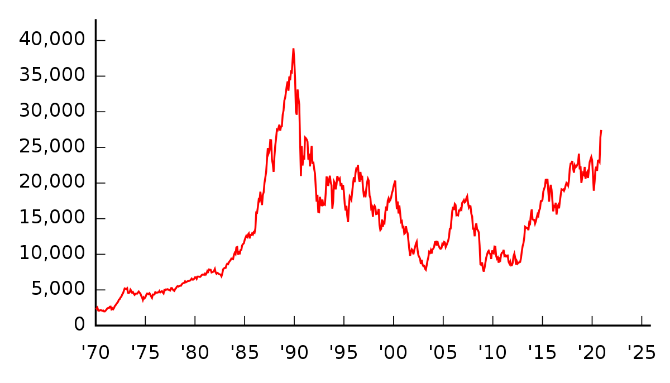

After WWII, the Americans fixed the dollar-yen exchange rate at 1 to 360. Until the beginning of the 1970s this exchange rate remained fixed, the outcome of the Bretton Woods Agreement, which was abandoned in 1972. By September 1985, when the Plaza Accord was signed, the yen had strengthened by more than one third to 235. Less than a year later, in July 1986, the yen was trading at around 160. This clearly led the Japanese central bank and government to compensate for the loss of economic growth with expansionary monetary and fiscal policies for an already euphoric securities and real estate market. From the Plaza Accord (September 1985) to the end of 1989, Japan’s stock and property markets tripled, creating one of the largest bubbles in history. When the bubble burst, the yen was trading at 125 to the dollar. 20 years earlier it was worth 360. Five years earlier it was 260. Today, 30 years after the bursting of the Japanese speculative bubble, despite a stagnant economy, the yen has remained extremely strong.

Without the Plaza Accord, Japan would not have embarked on expansionary monetary and fiscal policies at an already euphoric stage, and the bubble would not have existed or at least would not have been so large and difficult to reabsorb. Moreover, the weaker exchange rate would have helped the country to sustain the economy, whereas a strong exchange rate prompted corporate restructuring and cost cutting to maintain competitiveness, which in turn increased deflation.

Today, Japan is one of America’s great allies. A pillar against China’s overwhelming power in Asia. Its economy remains in deflation despite 30 years of super-expansionary fiscal and monetary policies. Its public debt is enormous, more than 2.5 times its GDP. It reached 100% of GDP in the late 1990s and more than doubled over the next 20 years. Over 40% of public debt and half of Japanese government bonds issued are in the hands of the Bank of Japan (BoJ), which, by not sterilising purchases, is effectively monetising the debt. Historically, monetising government debt has always led to significant currency devaluations. However, the yen remains strong driven by US and Chinese purchases and supported academically by not always effective exchange rate valuation methodologies, which mainly take into account the inflation differential. Major research houses such as JPM, Credit Suisse and GS, as well as various international institutions such as the IMF, consider the yen to be undervalued against the dollar. As mentioned, the calculation is based on valuation methodologies that mostly use the inflation differential of the various countries. Since Japan has been in deflation for 30 years, it is clear that its exchange rate is overvalued as a result. However, financial theory has to stop when faced with unknown and non-recurring circumstances (such as the state of constant deflation in which Japan finds itself) and should be able to be flexible.

Applying the above valuation methodologies to the yen and assuming that Japan continues to remain in a state of deflation and economic stagnation, it appears that its exchange rate must continue to appreciate indefinitely, thus, bringing further stagnation and deflation. All the way to where? Depression? And then what? In the real world, in order to avoid depression (and consequently default), Japan constantly applies expansionary fiscal policies that increase public debt. Public debt is methodically bought and monetized by the BoJ (actually the BoJ does not cancel it and therefore does not formally monetize it for now, but by not sterilizing the money supply it seems as if it does). This factor, the monetisation of debt, is not taken into account by the classical methodologies of exchange rate evaluation.

Let us try, in a simplified way, to incorporate it. Let’s take the “theoretical” USD/JPY exchange rate using an average of the most widely used classical methodologies (EER – Effective Exchange Rate and PPP – Purchase Power Parity), which is around 100 yen to the dollar. Let’s dilute this by considering the 45% or so of public debt held by the BoJ, which is equivalent to 35% of Japan’s M3 monetary base. Applying a 35% “dilution discount” to the exchange rate, we would arrive at a dollar-yen ratio of 1 to 135. Some 22% below current levels. A devaluation would allow the country to recover and make its debt, which is not yet in the BoJ’s hands, sustainable, then lay the foundations for a gradual normalisation of the exchange rate. The sooner the rebalancing takes place, the lower the risk of a violent and exaggerated adjustment.

The yen is called the “widow maker” in the financial market, referring to the number of traders who have fallen victim to the seemingly easy trade of betting on the devaluation of the currency, only to find themselves with large losses and the need to close their positions. Yet, what would happen if the yen depreciated? Today, much of Japan’s manufacturing output is concentrated in exporting countries. For this production, the benefit of a devaluation would only be in the higher value of profits made abroad. However, the production of high-tech goods is still in Japan. Generally, for a 10% devaluation of the yen, Japanese industrial companies benefit from a profit effect ranging from under 5% to over 30%, not a small amount. In addition, devaluation would inevitably lead to greater consumption of domestic goods, a greater influx of tourists and more investment from abroad. A gradual but significant devaluation, around 20-25% from current levels, would bring back some inflation in the country, some optimism among the citizens and an explosion in the stock market, perhaps the most undervalued in the world. Inflation and growth would also have a beneficial effect on the heavy public debt, gradually making it sustainable. Moreover, almost half of that debt, the debt held by the BoJ, could in fact be written off (and would set an interesting precedent for Europe and the US as well). After so much suffering, the Japanese situation must be put right and the mistakes made at the Plaza Hotel in 1985 at least partially corrected.

Logbook

Aegon largely beat expectations, even after deducting some positive non-recurring items. The improved operating result translated into good capital generation.  Despite the stock’s good reaction to the data, Aegon continues to trade at a steep discount in the insurance industry, an anomaly that seems to be more a legacy of past capital issues than a reflection of the current situation. The company trades at a P/E ’22 of 6.5x and a P/TBV of less than 0.4x. We believe that the process of divesting non-core assets together with no longer negative interest rate dynamics may lead to the emergence of this value.

Despite the stock’s good reaction to the data, Aegon continues to trade at a steep discount in the insurance industry, an anomaly that seems to be more a legacy of past capital issues than a reflection of the current situation. The company trades at a P/E ’22 of 6.5x and a P/TBV of less than 0.4x. We believe that the process of divesting non-core assets together with no longer negative interest rate dynamics may lead to the emergence of this value.

Delfi, one of the leading producers of chocolate confectionery in Indonesia, closed the quarter with a recovery in sales (+3.6% at constant exchange rates), still limited by the new lockdowns that hit the country in the second quarter. In this context, management has focused on cash generation, strongly reducing debt through lower working capital (free cash flow of almost twice EBITDA). Delfi is trading at only 5 times normalised EBITDA, despite the structural growth of the Indonesian market and its financial soundness.

EON reported particularly good quarterly figures, buoyed by the recovery in demand post Covid and the absence of last year’s abnormal weather events, with positive repercussions in all divisions. The upward revision of guidance was expected, mainly due to a non-recurring gain (agreement with the German government to settle the well-known nuclear dispute). The stock reacted positively to the supportive news flow, but continues to show low valuations due to its essentially regulated nature (EV/EBITDA ’22 around 8x). Valuing the regulated component (75%) with Terna’s multiples and the rest at 7x EBITDA gives an upside of over 50%.

Postnl provided a pleasant surprise, not only in terms of quarterly results, but also in terms of significant improvements in medium-term earnings targets (2024), above the values incorporated in analysts’ forecasts, some of whom believe that this company may have already reached peak earnings. The growth driver remains the spread of e-commerce. Management assumes that the parcel delivery division could see further revenue growth of 11/13% over the 2022-2024 period, compared to a recent and passing 8% decline in the postal division. The stock offers a dividend yield of close to 9%, which is also highly visible due to its debt-free financial structure. In addition, it is difficult to understand why the stock has not yet managed to return to the highs of late May in the €5 per share area.

SFA Engineering, a leading Korean company in the smart factory, semiconductor lines and EV battery manufacturing, reported a decline in operating profitability due to unfavourable exchange rate effects and lower conversions of orders into sales. However, orders were up almost 90% from the previous quarter, confirming acceleration in progress, which is expected to gain further momentum in the second half of the year as Korean EV battery manufacturers need to increase their production capacity (EV batteries are expected to account for around 25% of new orders). The stock was affected by the larger semiconductor equipment division, remaining an important cash cow, instrumental to investments in the battery division. The stock, which has returned to its beginning of the year level, has net cash equivalents to about 1/3 of its capitalisation and is trading at less than 10 times ’22 earnings.

Sumitomo Metal Mining, in spite of the negative stock market performance, reported figures above consensus expectations and raised earnings targets on the basis of conservative assumptions (assumptions of prices of some important metals well below current market levels). Virtually all divisions are contributing to the results, including the electric car battery materials division, demonstrating the validity of the integrated business model. The stock trades at a huge discount to larger copper businesses such as Freeport and at 1.1x tangible equity, which for a mining company renders it an anomaly. The company has no debt.

Toshiba reported strong results, with several divisions reporting better-than-expected figures. The guidance was not raised due to a cautious attitude towards the possible effects of chip shortages, increased costs of raw materials and logistics, which leaves room for possible positive surprises later in the year, when the picture regarding the expected changes in group governance will become clearer. In the meantime, the subsidiary Kioxia (formerly Toshiba Memory) is experiencing an extremely positive moment, certainly not surprising given the positive phase experienced by the semiconductor industry. The company is also an important producer of lithium cells for EVs, especially trains and buses.

Daiwa House. Japan’s largest operator in the residential construction sector reported strong figures, with 3% growth in sales and 6% in profits. The company also enjoys good geographical diversification with nearly 40% of its business overseas, most of which in the US and Australia. The company is solid, with debt/EBITDA of 1.4 (usd 6 bln debt) against an inventory of finished homes and work in progress of about usd 10 bln. It trades at around 9x this year’s earnings, almost 4% dividend and 1.2x tangible equity.

Aviva. One of the European insurance giants predominantly issuing life exposure reports, well and truly gives an encouraging update on its strategy, which resembles that of Aegon. The company is doing what many of the companies in the area we monitor, are supposed to do, value: if they can’t earn the cost of capital they must then restructure the business, focusing on where returns are highest, and return excess capital to shareholders. Out of £17bn of capitalisation, the company will return about £6bn to shareholders, including £4bn within the next year. The resulting company will be worth 7x earnings, pay over 5% dividends and operate in areas where it has enough critical mass to be very profitable. Since a significant portion will be paid back through buybacks, the company not only offers a good upside but also has some support for market turbulence.

Samsung Life. The Leading life insurer in Korea. The market environment is turning from dramatically negative to decent. Rates are rising, equity investments are growing and solidity is reaching remarkable levels. This is allowing for a generous distribution policy. Despite this, the company still has a ROE on ordinary operations of only about 3%, well reflected in the capitalisation to tangible equity ratio of 0.34x. Despite the strong recent performance, we believe this remains a very attractive restructuring story with very solid support and a good correlation to the Korean equity market (through proprietary investments and policies) and the economy (through rates).

Back